🔋Invest In Yourself - Pt. 1

The student loan stimulus is over, another cautionary tale.

If you found this article interesting, click the like button for me! I would greatly appreciate it :)

In March of 2020, payments and interest were paused on student loan payments. For three and a half years, fresh graduates and professionals alike were able to simply forget their student loans existed. For some, the hope of student loan forgiveness under Biden also became a topic of massive discussion. In September 2023, these hopes were officially quelled, as payments and interest started back up again. Courts and a looming election would thwart loan forgiveness efforts, pouring more salt on the wound for recent graduates hoping for a bailout.

The consumer economy has been deteriorating in aggregate, but nowhere near crisis levels. The unemployment rate at 4.3% remains at historically low levels. If everything is “fine,” why should we still be worried about the student loan issue?

For starters, many borrowers are simply not paying. Is this by choice, negligence, or necessity? According to government data, only one-third of the 38 million borrowers who should be making payments are. [1] Now, the Department of Education plans to collect on defaults, which they haven’t been doing until now.

The numbers are staggering. [2] There are 42.7 million borrowers, which comes to a total of $1.6 trillion in student debt. Nearly 10% of borrowers are currently in default, with another 15% in late-stage delinquency. Later this year, 25% of all student loans will be in default. This could reduce disposable incomes by $3-9 billion.

The median/average student loan payment is ~$500, a tremendous stimulus to the economy over the last 5 years. This could allow that money to go towards things like consumer goods/services, the stock market, other debts, and savings. It also isn’t just lazy young people with student loan debt asking for a bailout. All age groups still have significant student loan debt and have increasing delinquency rates.

That $1.6 trillion of total student loan debt only represents 9% of all consumer debt, but it is especially harmful for younger folks holding less assets. It also carries a significant spillover risk to other debt markets, which may be big enough to affect the aggregate economy. If people can’t make their student loan payments, it becomes more likely that they cannot pay their credit card and auto loans.

Auto loans are something that someone fresh out of college may look to take on. Subprime auto loan delinquencies have been rising since 2021. This is an area that could see spillover from an unsolved student debt burden. With high interest rates and a lack of affordable used cars on the market, more borrowers may feel pressure on auto loans if their student loans continue to present hardship.

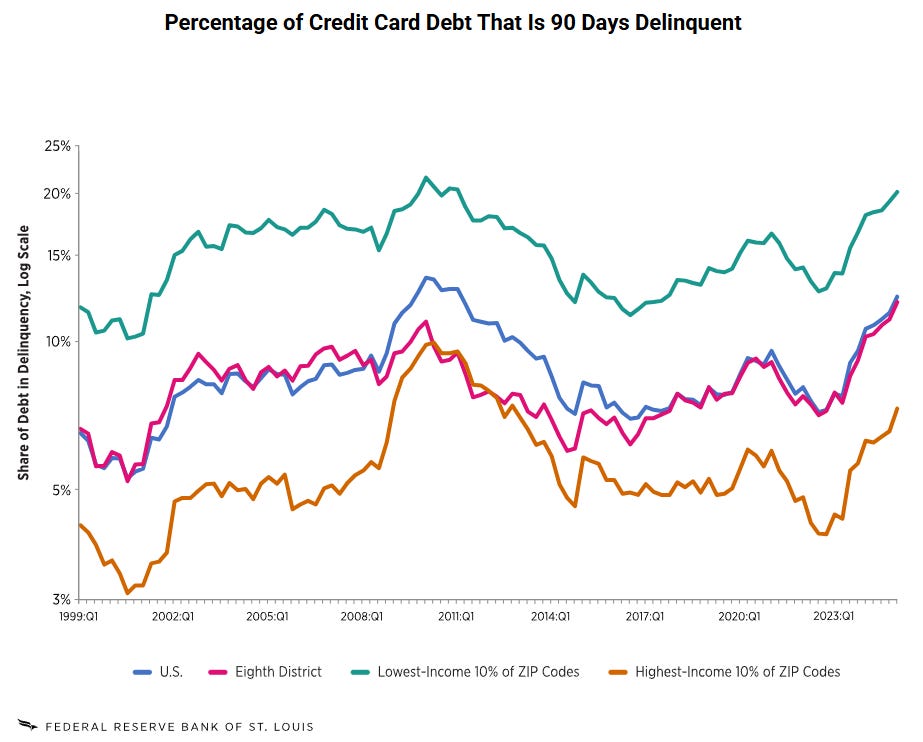

With the return of student loans, some may have to draw on savings and even credit cards to afford their lifestyle. Delinquent credit card debt for all income ranges has been increasing since 2023. Spillover into credit card debt is very pernicious at 20% interest rates, common for credit card debt.

Increasing delinquency is an early sign of recession or economic slowdown. Only once the unemployment rate increases significantly will these debts become serious issues, since people won’t have incomes to support their debts. The student loan pause over the last 5 years was a significant economic stimulus. While helping in the short run, it caused a malaise in borrowers who used it to consume, as seen by the personal savings rate.

Biden was the candidate advocating for the cancellation of student loans, and the election of Trump tanked any hopes of the legislation going through. One radical take would be that Trump himself may do a 180 and consider student loan relief sometime if we enter a recession. No debt class matches his populist base better than US citizens who qualify for direct federal student loans. Direct checks to households may have seemed unlikely under Trump, but we got that. Direct public bailout of mortgage, auto, and credit card debt seems unlikely, but student loans may be the most palpable politically. There are decades of crony bank and corporate bailouts by the federal government, building resentment in the working class. If things go downhill and Trump decides to appease the masses instead of Washington, what better path than to finish what Biden started?

I don’t have high conviction in that take, but it is something that I could see that many wouldn’t expect. Even if it helps Main Street instead of Wall Street, a bailout still doesn’t address the real problems that caused the student loan mess in the first place. Until next week,

-Grayson

Leave a like and let me know what you think!

If you haven’t already, follow me on Twitter/X @graysonhoteling and check out my latest post on notes.

Socials

Twitter/X - @graysonhoteling

LinkedIn - Grayson Hoteling

Archive - The Gray Area

Let someone know about The Gray Area and spread the word!

Thanks for reading The Gray Area! Subscribe for free to receive new posts and support my work.