🔋Not Your Dollars

A successful and fruitful re-industrialization of America has a scary unintended side effect.

If you found this article interesting, click the like button for me! I would greatly appreciate it :)

Trump suggests that the US trade deficit is unbalanced and unfair. I argue that everything is always in balance, and the US got exactly what it signed up for. Even if Trump realizes the US can’t have its cake and eat it too, he won’t tell you what happens next.

In 1913, the Federal Reserve became the central bank of the US. Following WWII in 1944, the US took on the responsibility of holding the reserve currency. Global trade went through dollars, and the Federal Reserve became the de facto backstop of liquidity and banks worldwide. With a soft gold backing to the dollar, this only worked until gold was rushing out of US vaults. In 1971, Nixon severed the gold standard “temporarily,” which meant the US defaulted on its debt obligations. Since then, paper money has been created by banks without any backing by real assets.

As the world globalized, US dollars were needed for trade, and other countries began looking for ways to create their dollars offshore or attempt to get off the dollar system. The misadventures in the Middle East were in large part to preserve the dominance and hegemony of the US dollar for global trade. Oil is the world’s most precious resource, and without trade occurring in dollars, there was little value. The Iraq and Afghanistan wars may seem like a failure, but they succeeded in controlling the region’s trade activity and maintaining dollar oil trade.

With globalization increasing rapidly with the modernization of China and the newfound strength of the petrodollar regime, the dollar was demanded all around the world at an excessive scale. To facilitate trade, the US needed to supply adequate liquidity to foreign markets to ensure stable trade. The strength and exports of dollars came at the cost of US exports and industrial capacity as it became cheaper to make things in foreign countries and import them rather than make them in the US.

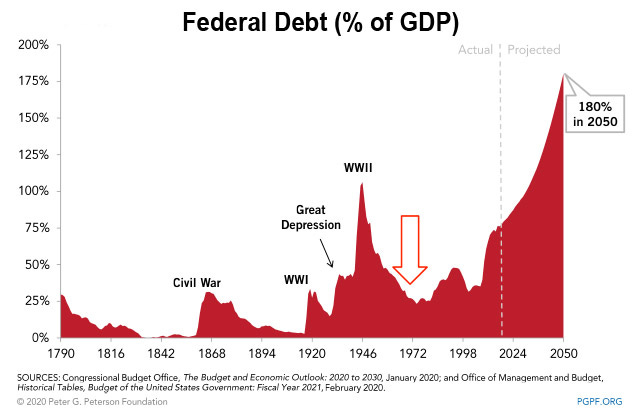

Many have benefitted from this scenario, while many in the US have not. Trump has taken his election as a reason to address this issue. The federal deficit has blown out, starting in 1971 when the US could begin exporting dollars without fiscal restraint. This rapidly increased with the globaliztion period at the turn of the century, with the most significant being the broad inclusion of China in global trade.

What Trump may not realize is that with the reserve currency comes a structural bid for global debt. This assumes he isn’t bolder than any of us realize and doesn’t want reserve currency anymore. With foreign companies selling goods in dollars to the US and rest of world, there becomes a balance of dollars overseas. Instead of letting the dollars rot away and lose value, countries and companies look to re-invest. The easiest and safest place to park dollar cash is with the US government with treasury bonds. US bonds are synonymous with US debt, which has risen exponentially since 1971. Even as a percentage of GDP, the federal debt has exploded higher.

As you would expect for the reasons I just mentioned, the foreign share of debt has increased over this time frame from 9% to 29%. Until now, this has mattered very little. If Trump is serious about tackling the trade deficit, which it seems like he is, the share of global debt owned by foreign borrowers becomes more important.

I am not here to argue the morality or necessity of reducing the trade deficit. Even if you support the idea of tariffs or other measures to reduce the trade deficit and bring industry back to the US, and that is a good thing, there will be other side effects that cannot be ignored. Like I said earlier, the surplus dollar profits of foreign nations get recycled back into US bonds and equities as a hedge against debasement. This is a massive demand for these assets, and when the demand curve shifts lower, prices also go lower.

Foreign investors own 29% of US treasuries and 18% of US stocks. Without profits from trade surpluses, foreigners cannot maintain their pace of purchases of US assets. Furthermore, in an environment with a hostile US trade stance, many countries may choose to divest in favor of other investments or position trade away from the US because of the newfound risks.

The consequence of this is that lower capital inflows into US assets would be negative for the prices of stocks and bonds. The stock market has been performing exceptionally well, and this could be a headwind instead of a tailwind. Further, with less demand for US debt, the US must balance its budget or find other buyers for the debt. While DOGE is nobily trying to cut US spending, for reasons I’ve discussed, I think they will be unsuccessful in making a dent in US fiscal deficits. Without tax increases, monumental tariff income, or fiscal restraint, the US Federal Reserve will have no choice but to monetize the debt and increase its balance sheet, similar to the post-2008 financial crisis and the many quantitative easing periods that followed.

It sounds good from a domestic economy and security perspective to bring industry and manufacturing back to America. People don’t realize or must accept that the consequence to that is saying goodbye to their precious stock market returns and don’t expect bonds to perform as a hedge. Until next week,

-Grayson

Leave a like and let me know what you think!

If you haven’t already, follow me at TwitterX @graysonhoteling and check out my latest post on notes.

Socials

Twitter/X - @graysonhoteling

LinkedIn - Grayson Hoteling

Archive - The Gray Area

Let someone know about The Gray Area and spread the word!

Thanks for reading The Gray Area! Subscribe for free to receive new posts and support my work.

From what I've been reading, ultimately the US economy, and others, is going to have to default or hyperinflate to reset to a manageable deficit. DOGE seems to be taking an axe to institutions with a liberal bias (NOAA, NFS) or in some cases to those which are already running efficiently (Social Security has very low overhead despite it being massively underfunded). Returning manufacturing can't happen fast enough to grow the economy nor can the government be cut enough to stem the deficit. And with proposed tax cuts and big spending proposals by Trump I don't see the logic (and sending everyone a $5,000 check for DOGE efficiency cuts, talk about oxymoronic). But Trump may be reckless enough to cause a global collapse which ultimately may be our way out of this, some sort of debt forgiveness that desperation can bring.

Any thoughts on the idea that Trump is doing this intentionally to get the Fed to bring about lower rates during his term? Pressure on the economy means the Fed lowers rates, then he gets to refinance massive amount of bonds that are due at lower rates. This would benefit him for the rest of his term as generally lower rates lead to growth. Equities and other forms of risk capital then sky rocket