🔋The Fed's Climate

High interest rates could be bad for climate change - the aggressive rate hiking campaign has stuck a big blow to climate change companies and projects over the last few months.

If you found this article interesting, click the like button for me! I would greatly appreciate it :)

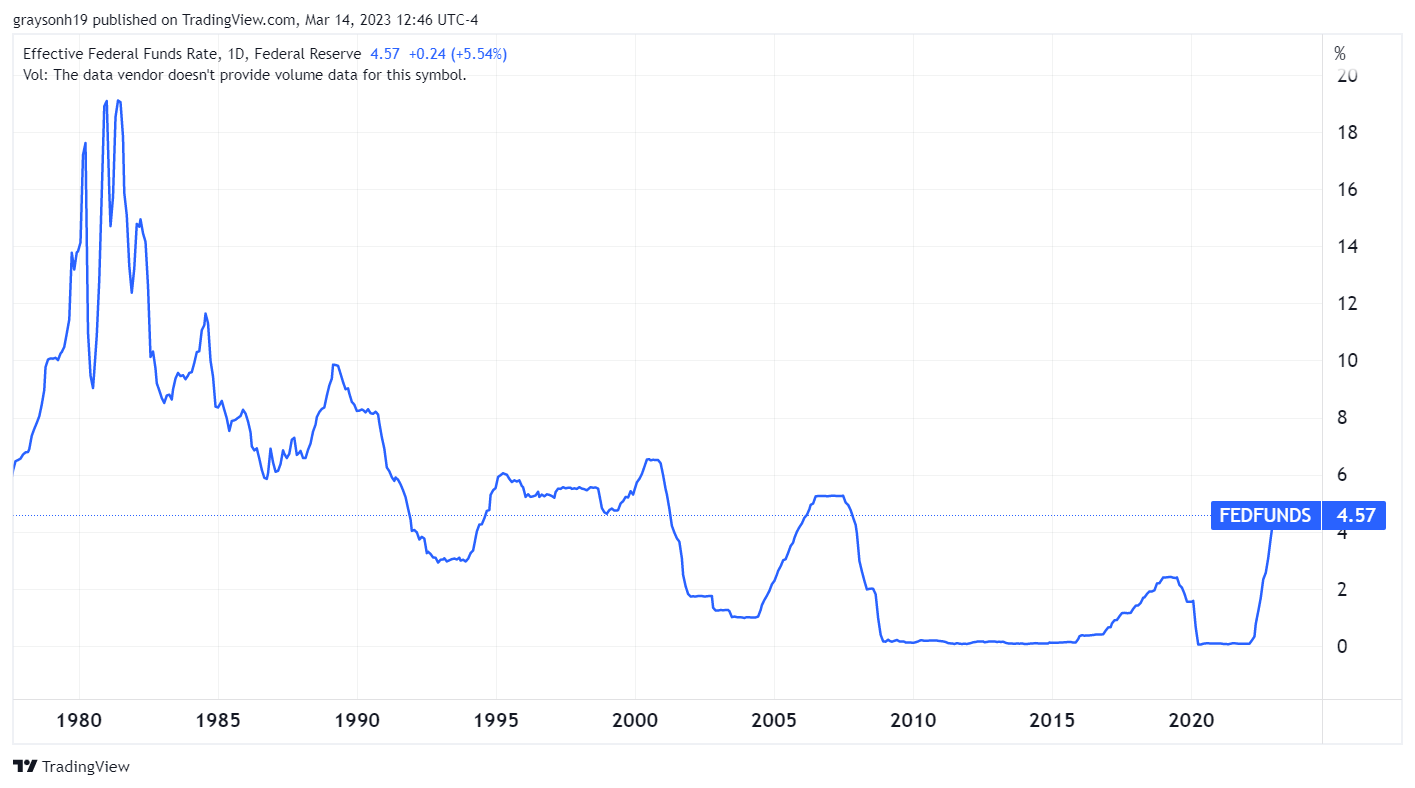

All eyes in the financial world today are on the Federal Reserve. With the power to set interest rates and lend more dollars into the economy, they seem to hold an almost omnipotent lever on the whole economy. The Fed has been on the most aggressive rate hiking campaign since the late 1970s/early 1980s when slaying the inflation dragon of the time. They do this by raising the federal funds rate which in turn influences all other interest rates. Today, poised for not to not repeat the same mistakes as the early 1970s, the Fed says it is committed to keeping interest rates off the zero percent floor for a while.

These interest rate hikes couldn’t come at a worse time for renewables developers and the climate change movement as a whole. These projects as well as new companies need large lenders to provide funding, which now comes with a higher cost. While it is true that there is a tremendous amount of new funding with the Inflation Reduction Act and Infrastructure Bill for clean energy, as a whole, the financial environment is much tighter than it was in years prior. Structural lack of funding in traditional energy sources has contributed to higher energy prices. In turn, we are at a crux of needing more investment into any and all energy sources and the reality that inflation and the higher interest rates have made it more difficult today. The IEA published a report saying about half the increase in clean energy spending is due to rising prices rather than investments in new clean energy capacity. In addition, I wrote back in January how US offshore wind projects were struggling to find and retain funding partners in The Cold Wind Blows.

Cracks are beginning to form on the corporate side which was seen in January as well with the shocking news of Britishvolt’s collapse, a company with plans for battery production in the UK. While overseas, the Bank of England shares a similar interest rate policy to the US Federal Reserve. While there’s more to blame than interest rates here, cost of capital is a startup’s best friend or worst enemy depending on how hard it is to get. Perhaps that hits home a little too hard here in the states with the progression of recent events around the collapse of Silicon Valley Bank (SVB).

SVB was the premier bank for startups and venture capital in the San Francisco area. As such, it provided a lot of funding for not only famous tech companies, but companies focused on climate change. The collapse was a combination of a classic bank run, being poorly run, and being over-exposed to sensitive equity/interest rate parts of the economy. From Heatmap,

The bank’s website bragged about its particular support of solar, hydrogen, and energy-storage companies. It provided more than half a billion dollars in revolving credit to Sunrun, the country’s largest residential solar company. (Sunrun did not respond to a request for comment by press time.)

And more than 60 percent of community solar financing nationwide involved SVB in some capacity, the bank claimed on its website.

The bank also published influential annual reports on the climate-tech sector, and it sponsored events for climate VCs and startups

It has become clear that the current climate tech movement has been impeded by higher interest rates. Whether this will have true far reaching impacts on the climate will remain to be seen, but the current path of this movement has come across another obstacle. Without government funding, projects are struggling to get off the ground in this environment.

Most people would probably agree that the zero interest rate policy that has been dominant for much of the decade seems like it doesn’t make a lot of sense, even if it has provided some nice boosts to asset values and allowed people to get a cheap mortgage rate. While raising interest rates is likely working to re-balance the excesses/froth in the economy, it undoubtedly causes disruptions which have already started. Bank failures and company bankruptcies are never fun topics, especially for those of us in the energy and climate tech space.

My point is not that these interest rates hikes are necessarily bad or that these banks/companies should be bailed out by the government, but that these forces have major implications for the companies, people, and the world going forward. It is entirely possible, likely even, that some companies would never have existed in the first place without interest rates at zero for so long. Should companies/banks get a bailout knowing that is the case? Moral hazard? Was zero interest rates the true bearer of pain? It is at the end of the day a shame that today, the pain of these collapses have to be felt by many involved and that arbitrary government policy was the arbiter of their fate. Until next week,

-Grayson

Leave a like and let me know what you think!

If you haven’t already, follow me at twitter @graysonhoteling and check out my latest posts.

Let someone know about Better Batteries and spread the word!

Socials

Twitter - @graysonhoteling

LinkedIn - Grayson Hoteling

Email - betterbatteries.substack@gmail.com

Archive - https://betterbatteries.substack.com/archive

Subscribe to Better Batteries

Please like and comment to let me know what you think. Join me by signing up below.

In regard to SVB...From what I've learned, SVB made a number of poor choices in organizations they backed. Maybe more crippling is that only one board member had banking background while others were added for "fashionable" reasons and decisions were based more on political agenda and the day's "what's fashionable" talk than historical business practice. Maybe a good way to sum it up is 'go woke. go broke' I expect to see more dominoes fall or rethink their corporate strategy as time goes on. On interest rates, they can make or break an economy, business or personal wealth. Generally speaking, lower rates that allow money to flow helps an economy grow. Higher rates can shrink it. While many see today's rates as high, they are really at a historical average and probably about where they need to be. Five to six percent is probably a range to stabilize things.

Those low rates allowed many marginal operations to use up resources in a less than optimal way. Some ideas are simply not economically prudent and actually dilute the market. So creative destruction is now at work. Has both good and bad effects.