🔋Debt Pt 5 - De-globalization

Fiscal deficits are rising - interest rates are not the policy miracle to solve inflation amidst new de-globalization trends.

If you found this article interesting, click the like button for me! I would greatly appreciate it :)

Re-shoring

One of the emerging buzzwords of late is reshoring or onshoring of industrial capacity. Perhaps seen most clearly in federal policies, but also seen in the corporate world. In the last few years, businesses have less trust in supply chains and geopolitical uncertainty is a looming concern. The idea of bringing manufacturing capacity back to the United States is not a trend we’ve seen before, but is becoming an area of emphasis on the corporate and government level as of late.

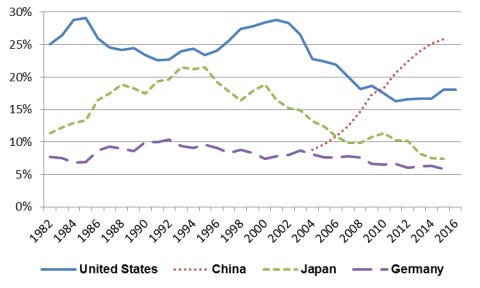

Manufacturing was once the dominant sector of the US economy, but the prevailing offshoring trend accelerated around the year 2000 in earnest. For the last 20 years, the focus was more on efficiency and cost competition than redundancy and security. The chart below shows the percent of manufacturing value added for the global economy. You can clearly see US and Japan be replaced by China since the turn of the century. This trend is very apparent to the real world experience as many things are made in China or overseas instead of domestically. This extends to things like medical supplies and even critical raw materials, which leaves the US at a disadvantage during any cold or hot war scenario. A change of this 20 year trend would be to tough swing in the other direction and would sure to cause some friction and distortions alike to spinning a cruise ship or semi truck around.

‘Less friendly nations’ to the US pose geopolitical security risks and there seems to be an increasing amount of dissent if you will from the US hegemony. Whether it be foreign holdings of US treasuries or expansion of the BRICS economic coalition, or outright sanctions on nations, the US is in a spot where it may not be able to rely on all of the supply chains it is used to. For example, the White House considers battery materials, uranium, and rare earth metals a security risk. Russia and China make up a large share of the market for these materials, raising concerns due to the cold/trade wars that have been waged. Further, oil supply can be used as a weapon by Saudi Arabia and other members of OPEC since it is still a vital component to energy and we rely on significant imports in the US.

De-globalization/re-industrialization in the US is not optimal in terms of economic efficiency and keeping costs low. An IMF report suggest that GDP losses could be significant under various economic decoupling scenarios. This adds credence to my assertion last week about free trade being the most productive strategy in total. Even if one believes that certain countries use bad tactics or try to gain unfair advantages, this report suggests that it is still a net negative to productivity to deglobalize. By limiting the available trading partners, the optimal trades may not be available, and the lowest price may not be on the table. This of course comes as companies and the government view some trading partners as unreliable, untrustworthy, etc. Reshoring is what takes place when security matters over efficiency, and in the long run that means higher prices. Because infrastructure is duplicated and not all resources are available to use, de-globalization has an inflationary tilt regardless if better technologies and techniques can be implemented in factories to mitigate it.

Policy

Over the past 20 years, inflation stayed low regardless of the record low interest rates and exorbitant federal deficits (loose monetary and fiscal policy). The federal reserve has kept interest rates lower than the headline inflation rate for a significant part of this time frame, relating to a simulative mode searching for higher inflation. During this time, production gravitated to cheap overseas labor and predominantly cheap coal for energy all while inflation stayed away. With this backdrop gone, the US will find itself with the opposite problem, too much inflation.

The cheap money provided by the policy decisions has allowed new money to chase different sectors as well. The digital economy has become a larger share of the overall economy. As such, finance, software, and healthcare jobs are some of the most desirable. Skilled labor has been left to the wayside as I’ve mentioned before, which adds to the stress of such a re-industrialization transition. The lack of emphasis on energy, metals, manufacturing, and infrastructure around the world leads to a lack of supply of these key resources as well as a lack of supply of this sector specific labor that we are starting to need more of going forward.

To combat the current inflation, the Federal Reserve has raised interest rates and undergone quantitative tightening (selling bonds or letting them mature as opposed to buying them) which are effective tools for quelling bank lending and demand side inflation. The problem with this policy is it does nothing to solve the structural supply of any commodities. It may be even worse than that since the reduced prices from lower demand may mask the true underlying issues with supply and discourage exploration and investment needed in the long run. In addition, high interest rates are a drag a new investment opportunities because the cost of capital is higher for mining or manufacturing companies looking to take on debt.

In addition to all of that, interest rates are most effective during inflation caused by bank lending. Lyn Alden has written extensively about how current inflation is driving primarily by high deficit spending (think 1940s) rather than bank lending (think 1970s) which has already contracted significantly and wasn’t at unreasonable levels to begin with. In such cases, interest rates do little to quell inflation. In eras with high debt/GDP which we are in now, higher interest rates can actually exacerbate inflation through higher interest payments on the debt needed to be funded through even more fiscal deficits in addition to money flowing into the private sector from the government.

The spike from COVID stimulus served as a one time increase in money supply, and all else equal would have a transitory effect on inflation. The Federal reserve got a lot of flack for labeling inflation as transitory, but the structural deficit spending/debt issuance that the US was, is, and continues to do during the de-globalization trend is what they miss in contributing to lingering inflation. It may only be in appearance that the interest rate hikes are the driving factor to lowering inflation that we are seeing now. Many analysts think it will be hard for inflation to return to the 2% target absent a recession. The large debt the US has accumulated amongst the backdrop of zero inflation is starting to catch up. According to the government, now is the time to lever up on debt to fund factories, projects, and critical industries. However, this is not ideal fiscal policy timing amidst fiscal deficit driven inflation, higher borrowing costs with higher interest rates, and record interest payments from the pre-existing debt burden.

Conclusion

While I’m not arguing that the US should or should not pursue this strategy, the strategy is vital in understanding labor, energy, material, and economic impacts going forward. That being said, the government and the federal reserve are running opposite strategies at the moment. They don’t realize, or won’t publicly admit that the fiscal spending is coming at the wrong time in the inflation fight.

Low inflation over the last decade has been largely due to exporting manufacturing to to cheaper labor and energy overseas. This new re-shoring trend brings a lot of second order consequences that all of a sudden matter including lack of skilled labor, lack of cheap energy, and structural underinvestment in natural resources. Inflation (potentially confounded by recession) over the long run may be here to stay driven by the overarching fiscal deficits and de-globalization. Until next week.

-Grayson

Leave a like and let me know what you think!

If you haven’t already, follow me at twitter @graysonhoteling and check out my latest post on notes.

Let someone know about Better Batteries and spread the word!

Socials

Twitter - @graysonhoteling

LinkedIn - Grayson Hoteling

Email - betterbatteries.substack@gmail.com

Archive - https://betterbatteries.substack.com/archive

Subscribe to Better Batteries

Please like and comment to let me know what you think. Join me by signing up below.