🔋Going Direct

Direct lithium extraction has the potential to be a technological breakthrough, but it has some surprising implications.

If you found this article interesting, click the like button for me! I would greatly appreciate it :)

The lithium sector is an exciting new area for investors, and for good reason. The “white gold” is not rare, but is labeled one of the critical materials necessary for the energy transition. More specifically, higher demand for electric vehicles and stationary battery storage will require subsequent demand for raw materials including lithium. This has made investors go crazy over the metal in 2021/22 and it’s easy to get swept up in the projected 19% compound annual growth rate of the sector over the next 6 years. With the high demand and the scramble to get supply, were the lithium speculators right?

Lithium was assumed to be in short supply, so a logical step is to look at producers and new technologies to alleviate these supply pressures. These companies stand to benefit if they are producing at expected high prices. It is clear now that the market speculation is over and prices have returned to normal historic levels. That isn’t stopping many companies, including major oil companies from getting in on the lithium hype.

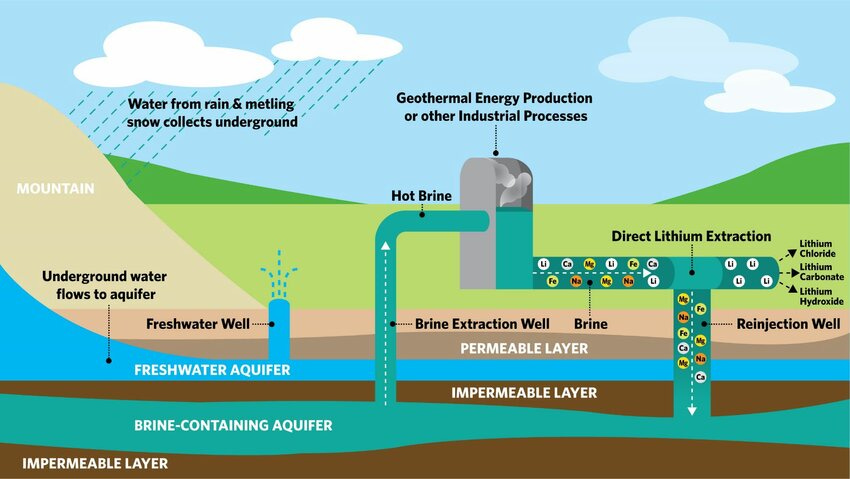

Even if new supply has responded to the short-term demand and the speculators have capitulated out of the market, that doesn’t necessarily mean that there isn’t a significant need for new long-term supplies of lithium. With many jurisdictions not friendly to traditional mining operations (not to mention the 10-20 years it often takes to permit mines), and saltwater brines restricted to certain geographies, direct lithium extraction (DLE) has become a buzz to hopefully revolutionize the lithium supply chain.

DLE refers to the refinement of brines into high-grade products and then re-injecting the waste brine back into the ground. If commercially viable, there are many advantages over traditional lithium mining.

Pros include less environmental impact, accessibility of lower grade brines/ other geographies than South America, non-weather dependent refinement (and faster), high recovery rates, lower water usage, and faster permitting process (10-20 years for regular mine).

Cons include its unproven economic viability, underestimated freshwater usage, high energy consumption, potential waste products, investor speculation, and the “shale problem.”

There are multiple types of DLE technologies, and each has additional pros and cons. See this review for a comprehensive guide to each technology and the current literature.

Adsorption

Ion-exchange

Membranes

Solvent Extraction

Some ion-exchange systems require acid and base chemical inputs which may be problematic at scale, membrane sourcing is a current bottleneck, and organic solvents for solvent extraction could be problematic at scale. In general, there is tremendous potential for this technology as seen below. If scale can be reached and bottlenecks resolved over time, DLE can cut land use, water consumption, environmental impact, permitting time, and potentially cost.

Many companies across all the various chemistry types are racing to commercialize their respective DLE technology. With the speculation that entered the lithium industry, there may be many companies or certain chemistries that are not successful in this endeavor, so caution is suggested when trying to pick winners and losers.

The “shale problem” is outlined eloquently by Doomberg, but essentially suggests that mining technology breakthroughs sow the seeds of their demise. The deflationary effect on lithium prices if the breakthrough occurs will put pressure on profit margins. This is seen clearly with the horizontal drilling breakthrough as natural gas prices in the US have come down considerably and many companies have not made it despite the shale revolution being an overall positive development.

IEA suggests that the increase in total mineral demand from current policy objectives is 2x, the sustainable development scenario (SDS) is 4x, and net zero is 4x. On top of that, 20-40x more battery materials are required by 2040 under the SDS scenario. With this in mind, multiple potential scenarios lay ahead.

Demand high as expected, supply low/trying to keep up: prices up - bull market in metals

Demand high as expected, supply high/able to keep up: rangebound price - if new mines come online or DLE technology takes off then the lithium price should remain lower

Demand lower than expected, supply low: rangebound price - if consumers or politicians lose appetitive for the energy transition, prices could fall even if the long-term supply picture is undersupplied of expected demand.

Demand lower than expected, supply high: prices lower - If we go into recession or consumers/politicians lose appetite for energy transition just as mines come online/new DLE technology is commercialized.

On top of this, we must consider the excessive deficits coming from governments around the world as debt burdens increase and the money printing to fund government liabilities is increasing at an exponential rate. This reduces the purchasing power of currencies and increases the price of commodities priced in currencies over the long run. If governments continue stepping in to subsidize certain metals or companies, it could further increase prices and stifle innovation. Also, an economy-wide recession can overpower these factors and push prices lower for some time.

I think blanket statements like there will be a supply glut or there will be a raging bull market in metals miss some nuance. Both of these scenarios are likely on different timeframes. In the near term, I expect economic weakness and the current supply glut to prohibit an explosion in prices as we saw in 2021/2022. On the longer-term scale, the supply challenges remain in the permitting of new mines required to meet the energy transition targets and excessive money printing suggests higher prices than in the last decade. Recycling, successful implementation of new technology like DLE, and more realistic expectations will result in prices likely not exploding into another speculative bubble. Until next week,

-Grayson

Leave a like and let me know what you think!

If you haven’t already, follow me at TwitterX @graysonhoteling and check out my latest post on notes.

Socials

Twitter/X - @graysonhoteling

LinkedIn - Grayson Hoteling

Archive - The Gray Area

Let someone know about The Gray Area and spread the word!