🔋Burst Your Bubble

What do commodity and asset bubbles mean for the future?

If you found this article interesting, click the like button for me! I would greatly appreciate it :)

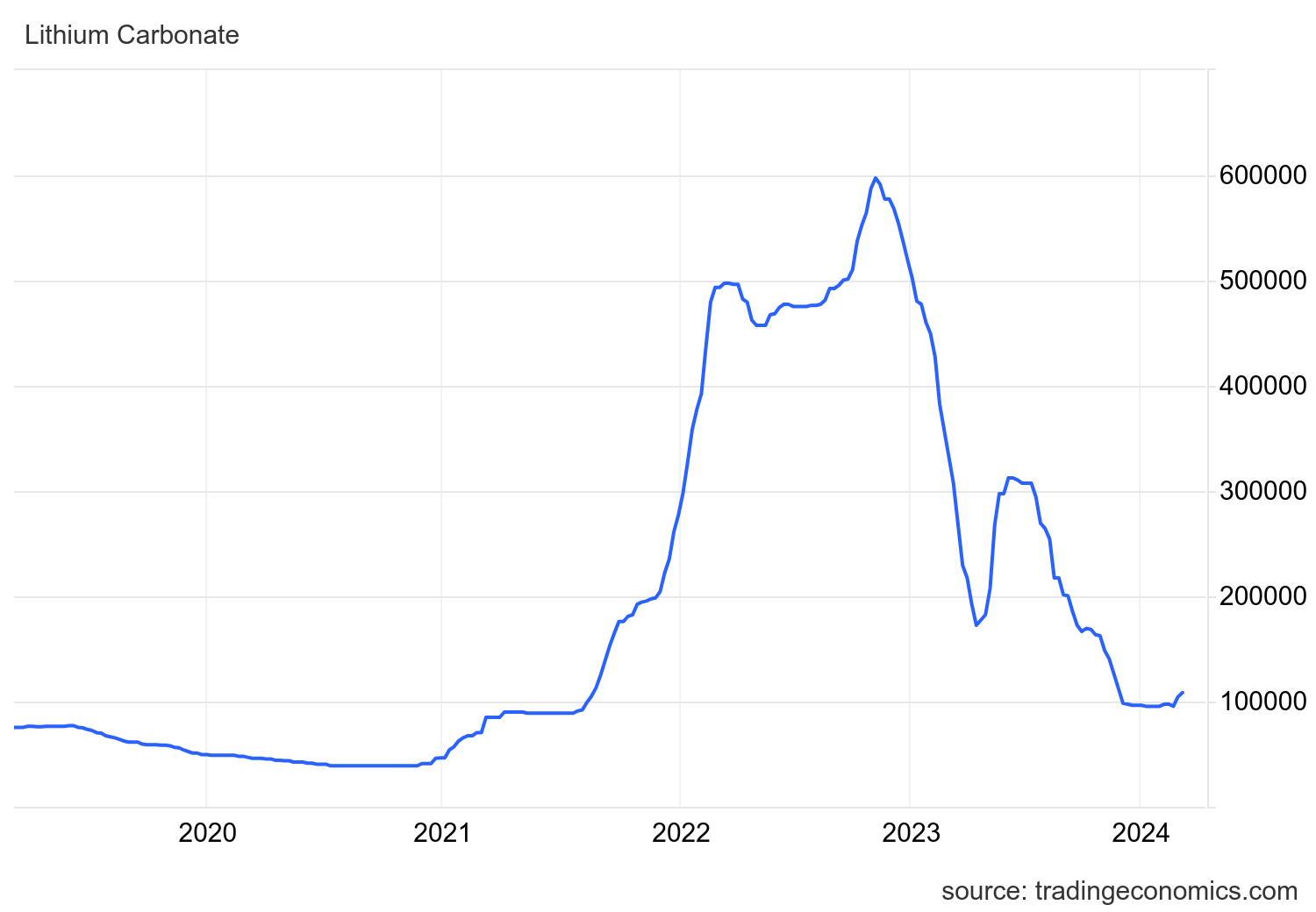

With just about everything in a bubble in 2021 and early 2022, that exuberance extended past stocks and into other forward-looking endeavors like the energy transition. With optimism about renewables and electric vehicles at all-time highs, the supply/demand balance for battery metals like lithium was concerning. The lithium price went up ~5x between Q3 2021 and Q2 2022, a remarkable move. Prices remained at astronomical levels through the end of 2022 where it has since retraced to 2021 levels in a similarly dramatic fashion.

Commodity markets tend to be much more volatile than other assets because of their increased dependence on supply as well as geographic considerations. Price spikes like this have occurred throughout history across asset classes. A few famous examples include the 1929 US, 1980s Japan, 2000 US stock market bubbles, the 2008 housing market bubble, the 1970s oil and gold spikes, and natural gas in Europe in 2022 among others. During them, human psychology makes it easy to fear uncertainty, fear missing out, and to think “This time is different.” What do these past bubbles/price spikes mean for assets like lithium or the stock market today?

Stocks

Some of the most impressive bubbles in history have been in the stock market. In 1929 the stock market was at record levels with rampant speculation before an ultimate crash that kicked off the great depression. At the turn of the century, the internet was rightly predicted to be world-changing, but this didn’t stop companies from becoming grossly overvalued relative to their profit-generating capabilities. One way to quantify the valuation of a company is using the cyclically adjusted price-to-earnings ratio.

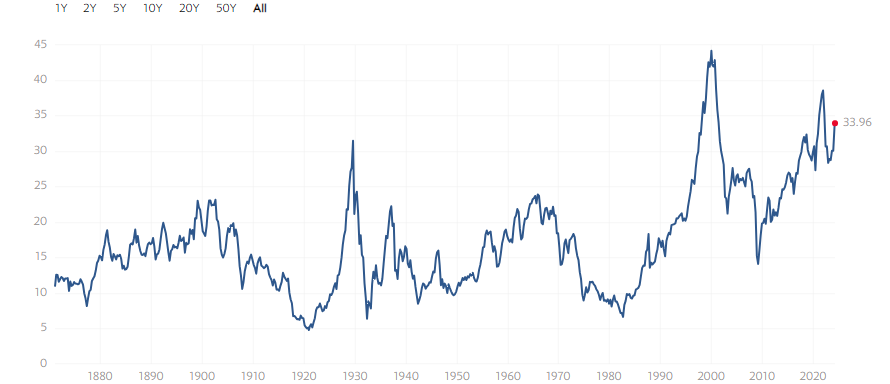

The cyclically adjusted price-to-earnings ratio (CAPE) ratio or Shiller PE Ratio is a valuation measure that uses real earnings per share (EPS) over a 10-year period to smooth out fluctuations in corporate profits that occur over different periods of a business cycle. Higher than average CAPE values imply lower than average long-term annual average returns. - Investopedia

Measuring the CAPE ratio over time is a useful tool to indicate episodes of over-exuberance in the market, but only over the long term. In the short term, momentum can drive markets higher and further than the CAPE ratio suggests stock prices “should” be. Currently, the stock market has a CAPE ratio of 34 which is a level only seen during the 1929 and 2000 bubbles. The S&P 500 has an average CAPE ratio of 17 over the course of history, implying that fair value would be close to 50% lower than current levels based solely on this metric.

High P/E ratios usually indicate an expensive stock market and are near tops which is seen below. In such cases, there are usually long periods of negative to flat returns in the market (accurately predicted by the CAPE ratio). This can be challenging for investors who rely on the stock market for income, retirement savings, etc. After 1929 it took 15 years just to break even if one bought at the top. Similarly, if you bought near the top in 2000, it would take 13 years to break even on your investment. This is a far cry from the stock market “always goes up” and the traditional advice to “sit and forget” about your stock investments.

Oil

While there’s no P/E ratio for commodities because there are no earnings, we can still look at price trends over time. Oil was on everyone’s mind in the 70s and remains the most important commodity to this day. With peaking US crude oil production, the severing of the gold standard, and conflict in the Middle East, oil prices went up nearly 5x during the 1970s adjusted for inflation. Interestingly, the Suez Canal was contentious real estate both then and today.

It wasn’t until 2008 (28 years later) that the oil price reclaimed its 1980 peak. The 2008 peak in itself has yet to be reclaimed as I write 16 years later. We can see that oil follows a similar and perhaps even more aggressive trend of blow-off top peaks and long dragged-out consolidations over years/decades.

Commodities

Commodities are not immune to the price spikes induced by abrupt changes in supply and demand which are inevitably exaggerated into bubbles through the greed/fear of human emotion. Ahead of 2008, Nickel began being used in Chinese steel production in addition to increasing demand in the global economy. While the great financial crisis sparked the popping of this commodity bubble initially, new steel production methods and new supply from Indonesia helped ease the price burden over the long term.

Interestingly, the post-bubble era still had higher prices than before the bubble. Similar bubbles have been observed with Silver in the early 80s, Zircon in the late 80s, agricultural products in the 2000s, and European natural gas in the 2020s.

Today

As far as commodities are concerned, high prices lead market participants to cut back on usage, look for alternative materials, and increase production to capitalize on high prices. This demand destruction and supply increase are responsible for the swift reversibility often seen in large price spikes. Many bubbles become solved naturally through these market forces, but sometimes the underlying issues are not fully addressed.

I’ve shown that prices tend to take a long time to reclaim past highs brought forth through a bubble or price spike which were inflated with speculation and investor emotion. While these peaks were exaggerated, many times the underlying concerns of supply issues in commodities mean that prices remain higher than previous historic levels.

Lithium and natural gas stand out as two commodities that have just come down from their blow-off tops. In both cases, supply worries have been alleviated in the short term. For lithium, if demand from the energy transition is to go forward, the underlying supply constraints remain over the long term absent a technological breakthrough. For natural gas, a mild winter, an aggressive LNG export regime from the US, and recession contribute to the recovery of natural gas prices. With the US less friendly to LNG exports, weather uncertainty, and potential economic recovery could mean that the root cause issues are not solved.

In both cases, there are new global supplies set to come online and new technologies hoping to breakthrough into the commercial spotlight. Other assets like the stock market have not popped yet. Regardless, there is a high likelihood it will take years to decades to reclaim previous bubble highs once they top. Until next week,

-Grayson

Leave a like and let me know what you think!

If you haven’t already, follow me at TwitterX @graysonhoteling and check out my latest post on notes.

Socials

Twitter/X - @graysonhoteling

LinkedIn - Grayson Hoteling

Archive - The Gray Area

Let someone know about The Gray Area and spread the word!