Leave a TIP

Bonds can protect you from recessions AND inflation?

If you find this article interesting, click the like button for me! I would greatly appreciate it :)

And How Do You Invest In Them? | Bankrate")

Many people are concerned with lasting inflation, and rightfully so. Since we hit 9% CPI in 2022, it has not returned to the Federal Reserves 2% target. Now, with Tariffs, oil shock from the war, record peacetime deficits, concerns about forever inflation are higher than ever. Inflation eats away at returns on assets, so if only there were a way to compensate for this.

Turns out there is, and they’re called TIPS (Treasury Inflation-Protected Securities). Yes, tipping culture is out of hand these days, but this is different. Treasury Inflation-Protected Securities. When you buy a TIPS, it pays a fixed yield on top of a variable principal that adjusts with CPI. This means that your bond yield is a “real yield” and you are not losing purchasing power on the bond. A regular nominal bond paying 4% with inflation that goes to 4%, you are making no money. However, a TIPS may pay you 2% on top of that 4% CPI, paying you 6% and ensuring you are ahead in real terms.

Just like nominal bonds, there is a price that has an inverse relationship to the bond yield. The real rate also fluctuates over time with market dynamics, meaning sometimes it is 0.5% and other times closer to 3%. So just like regular nominal bonds, you can treat them like cash to protect your money, or speculate on the price.

If you buy a TIPS from the treasury, you are guaranteed to return the principal at the maturity of the bond, even if there is deflation and CPI goes negative in a recession. However, owning TIPS ETF through a brokerage account increases your risk through marking to market every day. Are TIPS actually attractive given the current inflation worries?

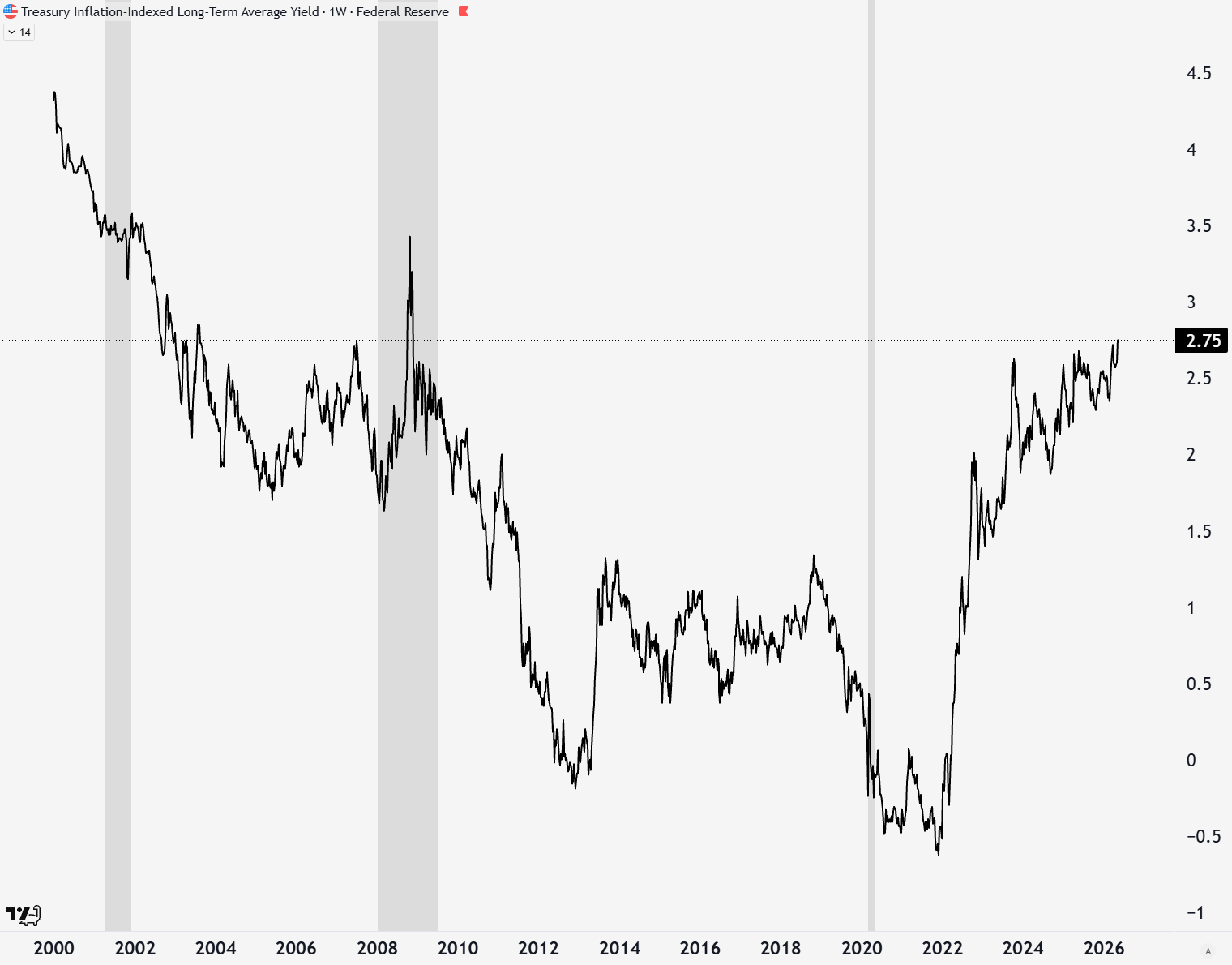

As of writing this, a 30yr TIPS is paying 2.71%. With CPI at 3.8%, the yield is ~6.6%. For comparison, the nominal 30yr yield is 5.14%, a whole 1.5% lower. Long-duration TIPS yields have not been this high since 2003 (and briefly in 2007/2008). Buying a real 2.71% for 30 years directly from the US Treasury is extremely attractive right now, especially given the stock market valuation's implied future returns and US deficits.

Macro

This means that macroeconomics is as important as ever. If we have no recession, recession, or stagflation, there are different implications for what to own and whether TIPS ETFs are attractive for trading. Personally, my research with The Gray Area leads me to believe that a recession of decent magnitude will be hard to avoid.

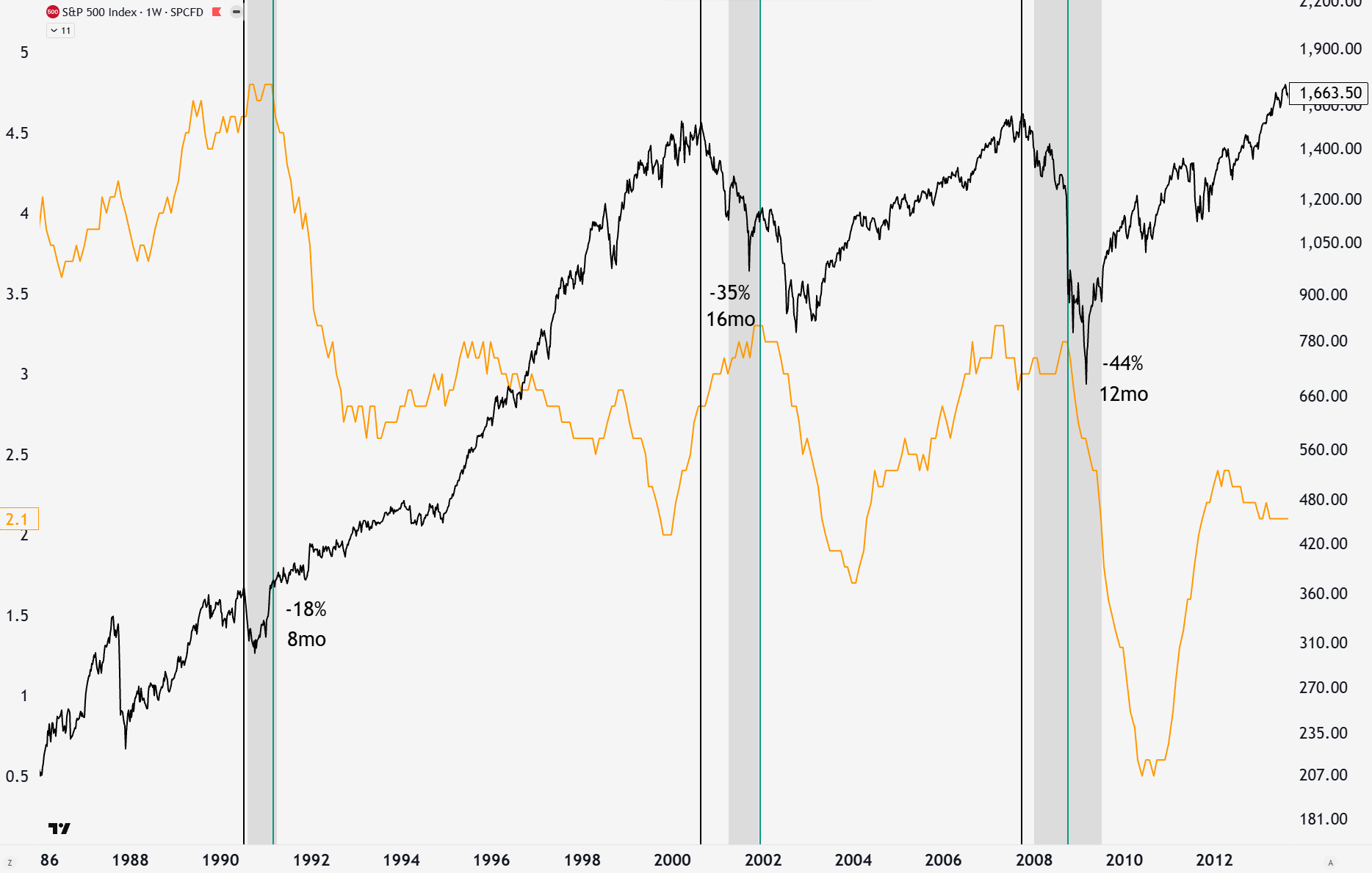

In a recession, inflation tends to give way to disinflation or deflation. This means that headline CPI goes down, but there is a lag in the data. In the 1990, 2000, and 2008 recessions, the stock market top preceded the CPI top by an average of 12 months with an average drawdown of 32% to that point. Additionally, the recession tends to be well established or nearly over before this occurs.

Market participants successfully predicted the top in inflation 4 months early in 2008 (10yr breakeven inflation rate). CPI data is notoriously lagging, as borne out by these two observations, but market participants don’t wait for CPI to decide what price they’ll pay for an inflation-protected bond. This is a simple math equation:

Breakeven inflation rate = Nominal 30Y yield − TIPS real yield.

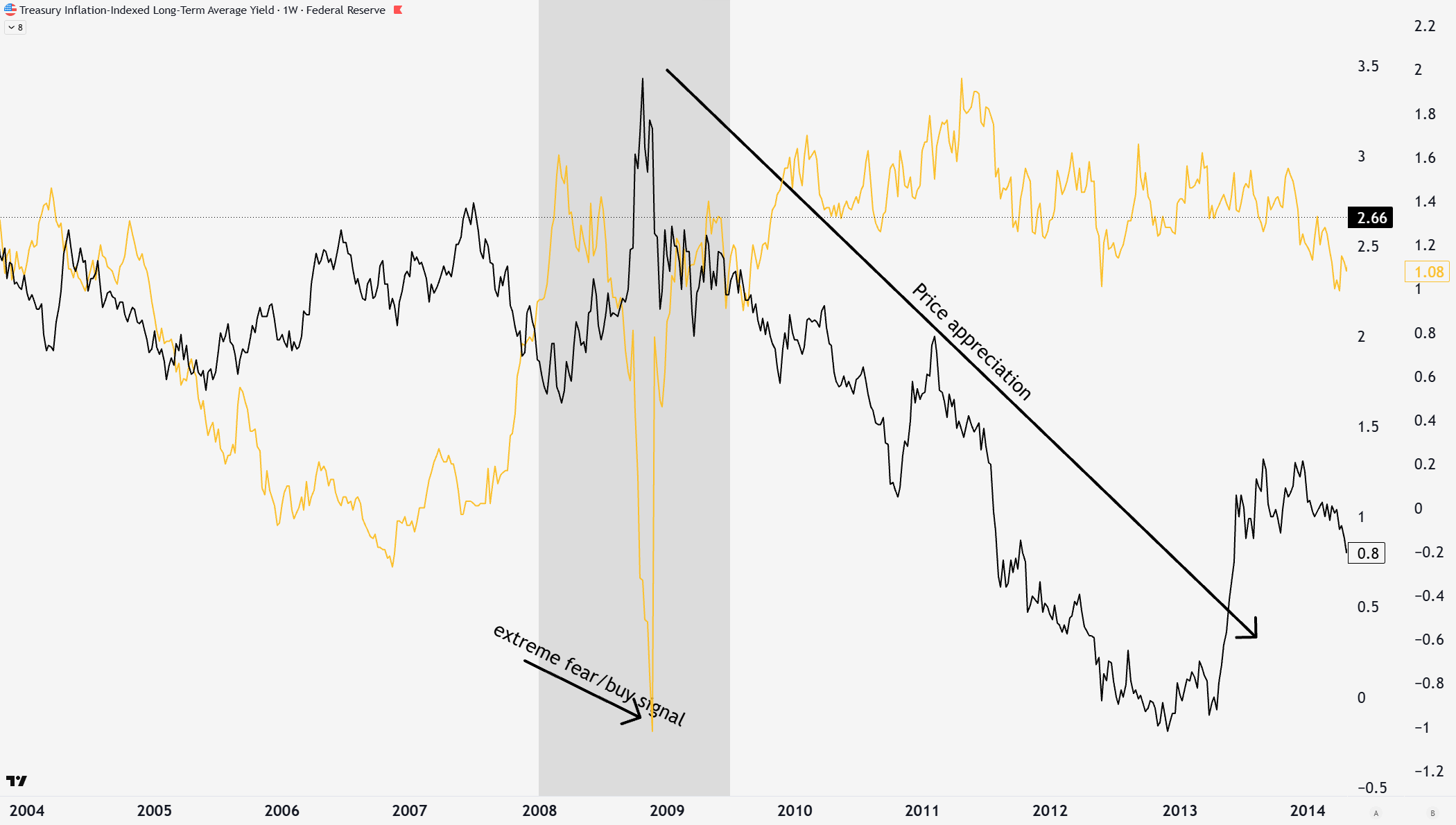

During a recession, there is typically a “blood in the streets” point where nearly all assets are sold to provide liquidity (flows into cash or bonds). Plus, sentiment for economic growth becomes extremely pessimistic. In 2008, TIPS were sold off in distress alongside stocks. This resulted in a harmful correction in longer-dated TIPS (longer duration bonds = more volatility). If you hold a TIPS from the treasury till maturity, you do not lose any principal, but losses can occur if you speculate on prices through ETFs.

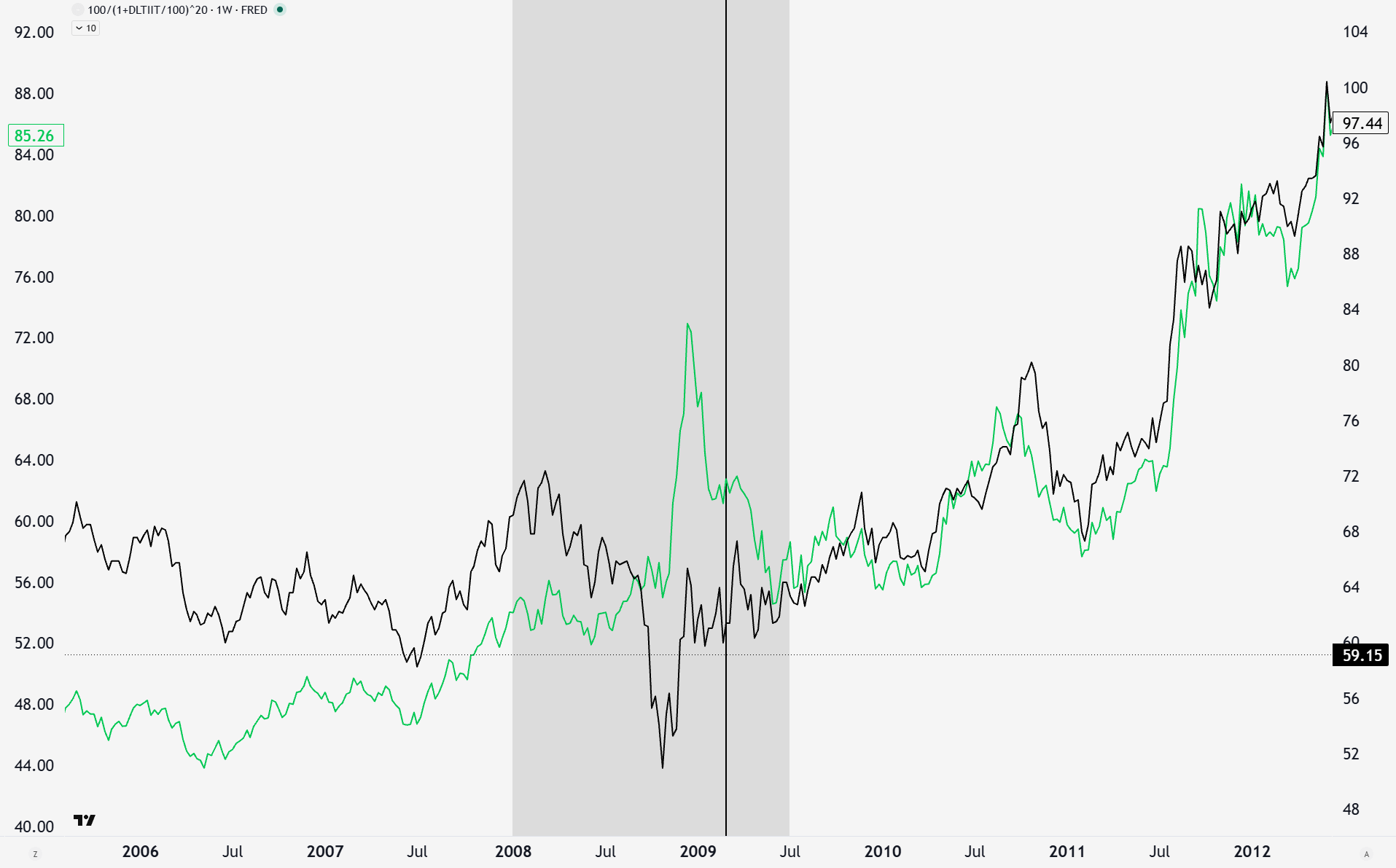

This can be seen in the real yield curve (ie, 20yr TIPS yield-5yr TIPS yield) in yellow. When the market puked in 2008, the real yield curve went negative instead of ~1 normally. This marked a good buying opportunity as people were liquidated and lost their minds with pessimism about the future. The spike in black either made you sweat about the value of the TIPS, or marked a great buying opportunity for incredible forward price returns (yields down = price up).

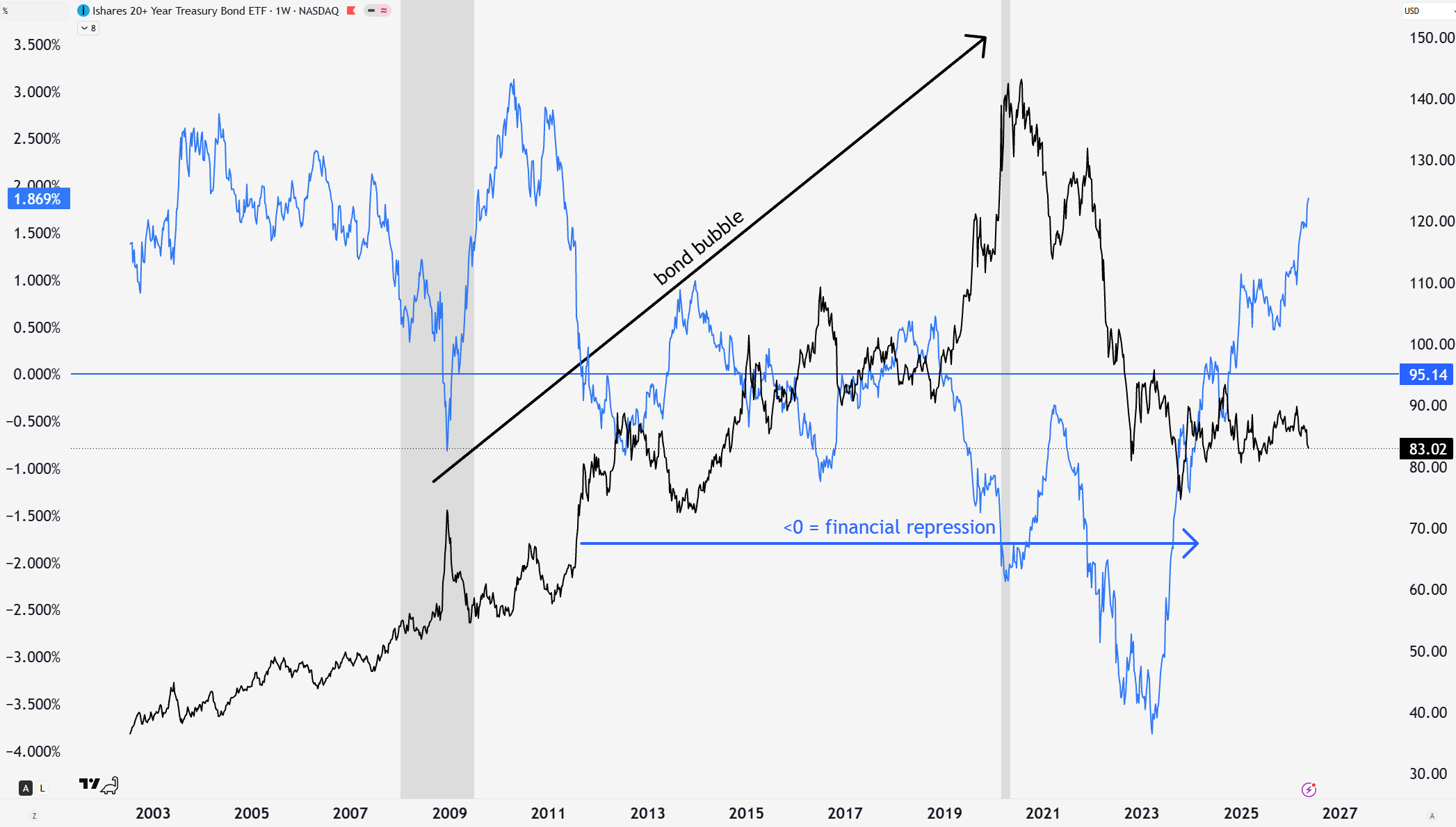

The reason the 60/40 portfolio exists and why you hold bonds is that they provide safety when the market goes awry. The long-duration nominal bond ETF (TLT) went up over 30% in 2008 while stocks crashed 50%. Bonds are boring until they aren’t. The problem, as we discussed, is that inflation eats away at nominal bonds, lowering your real return.

Plus, I discussed on May 20 in Tumultuous Times that the current fourth turning is likely to bring squirly behavior, including financial repression (negative real bond yields). We have largely already been under stealth financial repression since the post-financial crisis, only having a reprieve for the past year and a half. This means that bonds have been a horrible investment for the past decade from a yield/capital preservation perspective. If you were speculating on price, you could argue that bonds were in a bubble over that time and popped in 2021.

Making Money

Long-duration bonds are the single best asset to own during a deflationary episode like 2008. The problem today is that inflation and rising bond yields have people questioning their merits. Even with ~4.5% yield, that has only offset some of the losses in price over the past few years for price speculators. TIPS may offer an alternative, but not without its liquidity risk during a recession. This is why timing is important.

For a portfolio in a fourth turning, it is silly to hold TLT for a long time, which is why shifting to TIPS will be a good idea. With a paid subscription, you can see my exact bond portfolio allocation and plans, but essentially, I will shift TLT funds into TIPS after any deflationary/credit event episode.

You can see below that TLT outperformed in 2008 while stocks were puking and people were losing their minds. TIPS were not a safety play either, as they puked alongside stocks. However, catching the falling knife in TIPS is not as dangerous as stocks. This is because sentiment turns very poor and liquidations force people to sell in greater amount that the market may normally want to (also why gold goes down during this).

Inflation and economic growth will pick up again, despite calls for the end of the world, meaning TIPs will be a good investment at low prices. In this plan, TLT will provide the initial hedge against the stock bear market. Then, some cash will be used to purchase the TIPS at attractive prices. Then TLT will be sold for profit as the safety trade is over, and financial repression begins again through aggressive monetary and fiscal policy by the government. Owning TIPS instead of any nominal bonds or cash is then the only real way to have safety in the portfolio without the government stealthily taxing your money through inflation.

Where does this thesis go wrong? If there is no recession or stagflation. You can go back; much of my writing articulates why a recession is probable. Stagflation is overblown in today’s rhetoric, and sustained 7+% inflation would be less likely today. This is because the working-age population and labor force participation were increasing, driving nominal wage growth. Today, wage growth is declining, as we have the opposite case for both. Furthermore, much less of the economy is manufacturing/construction (other than data center buildout), which drives inflation of real things. Last, money creation was primarily bank lending to consumers and businesses, while today we have a higher share of unproductive debts. I do think we will have an inflation problem in the future, but I don’t think the inflation can stick as high as it did in the 1970s when the recession arrives.

Conclusion

The trade and timing may seem complicated, but it’s really not. We own long bonds because they go up while stocks get crushed in a recession. Shift the bonds to TIPS during the recession because once it’s over, they go back to underperformance, and TIPS still rise in price and simultaneously protect from inflation.

Bonds are a terrible asset to own in the long term, and I may look wrong in the short term, but the safety and outperformance when a recession hits will help me not get destroyed by the stock bubble bursting. Once the world freaks out, TIPS will be the move in the bond portfolio to avoid financial repression in the future. Until next week,

-Grayson

Like to see these asymmetric opportunities synthesized into a real model portfolio that beats the S&P 500 and avoids major downside risks?

Socials

Twitter/X - @graysonhoteling

Email - thegrayarea55@gmail.com

Archive - The Gray Area

Notes - The Gray Area

Promotions

Sign up for TradingView

For educational and entertainment purposes only. The Gray Area should not be taken as financial advice.