Oh Barnacles!

The least sexy trade of 2026 might also be the most obvious one.

If you find this article interesting, click the like button for me! I would greatly appreciate it :)

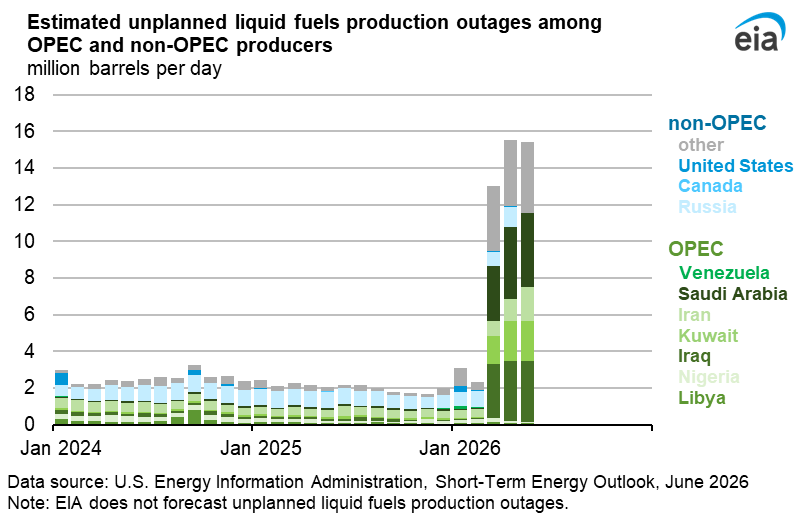

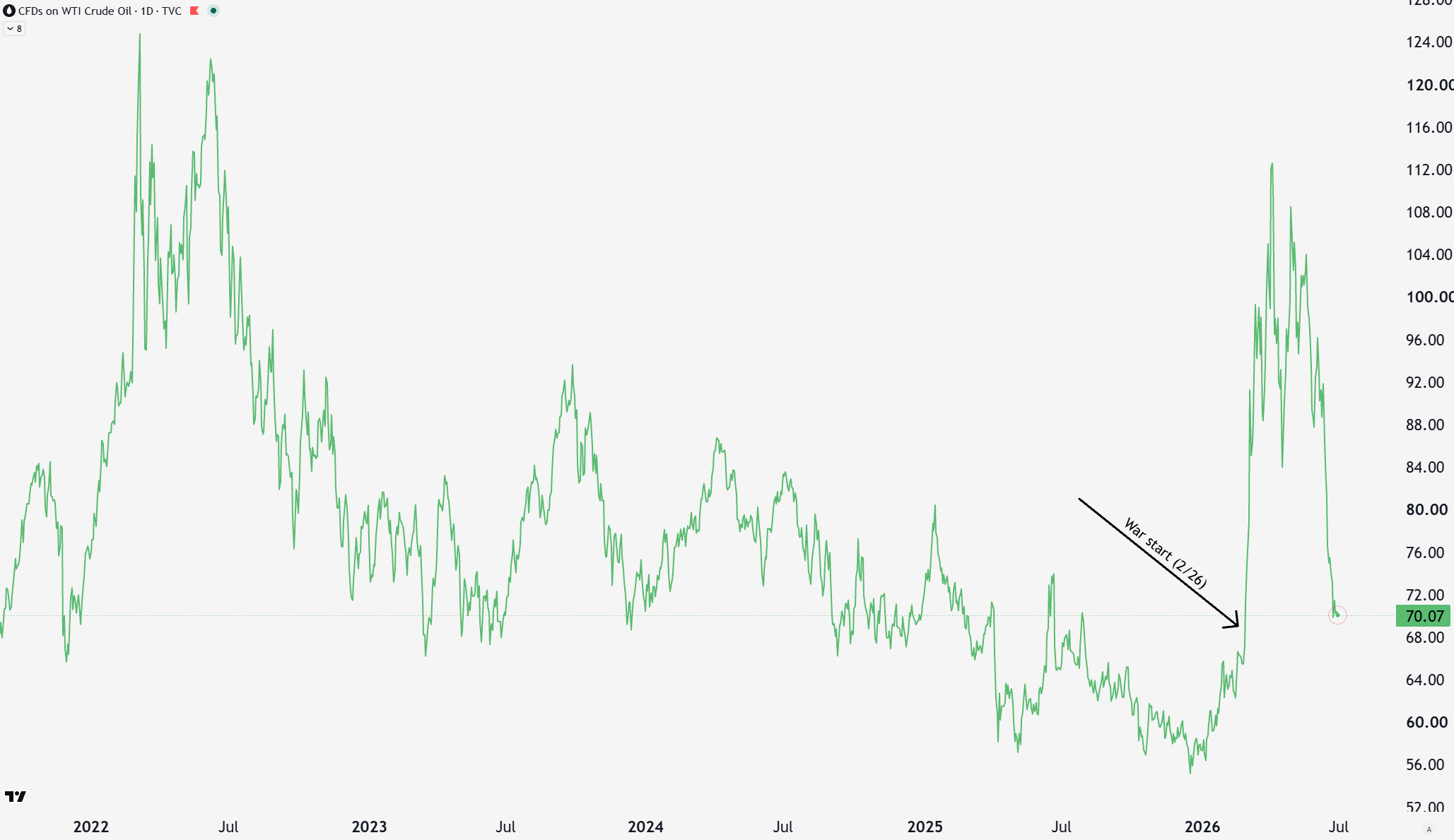

Peace to the Middle East, well, kind of. The US and Iran have signed a memorandum of understanding, but there have already been more strikes since. This article is not about politics, but energy. The disruption to the oil market from the prolonged closure of the Strait of Hormuz was not only significant in raising gasoline prices, but was the largest unplanned outage in history. Not only was it the largest disruption in terms of barrels per day, but also the largest in terms of cumulative barrels and percent of total global oil supplies. The 1979 Iranian revolution was the last time this happened, with prices going from $15 to $40/barrel.

If this was the biggest oil event in history, dwarfing measly events like the 2022 Russia war, why have prices not exceeded the 2022 levels? In fact, oil prices are already back down to pre-war levels. The peace deal helps a lot, but doesn’t magically make everything go back to the way it was before. The market is acting like everything is fine. Is it, or could we have ourselves a discount on an attractive investment opportunity?

Fundamentals

First, there are several concerns with the Straight of Hormuz. Even with the peace deal, some unknowns remain, such as whether it even holds. Strategic reserves and commercial inventories have been drawn down to record low levels. Not only does this leave nations less resilient, but it also raises questions about when these stop being drawn down and when they will be refilled.

Refineries are slow to ramp up/down production as well as switch to different types of oil. It may take some time to resume normalcy for refineries that were shuttered or switched crude sources. When wells get shut in and stop producing, it takes time to resume well pressure and resume full production capacity. This is the case for Iran and some other nations in the area. In some cases, wells never return to their pre-shuttered capabilities.

On top of these issues, shipping confidence, crew confidence, shipping insurance rates, and even barnacles will play a key role in resuming normal oil flows throughout the region.

With concern over the fate of oil in the Middle East, US oil is as important as ever. The US is the largest oil producer in the world, but that doesn’t mean that everything is back to normal after the reopening of the Strait of Hormuz.

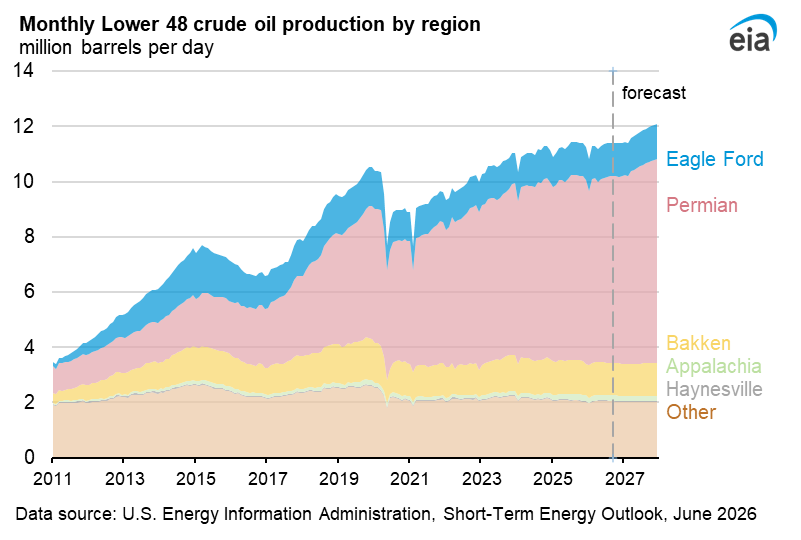

Despite projections for more drilling, US production looks to have peaked in 2025, on top of struggling to resume following the COVID disruption. The Permian basin region in Texas was pretty much the only region showing incremental production growth, and it has also shown signs of peaking out. This is not doom and gloom or a peak oil prediction, which never works, but shows that things are slowing and not as easy as they were.

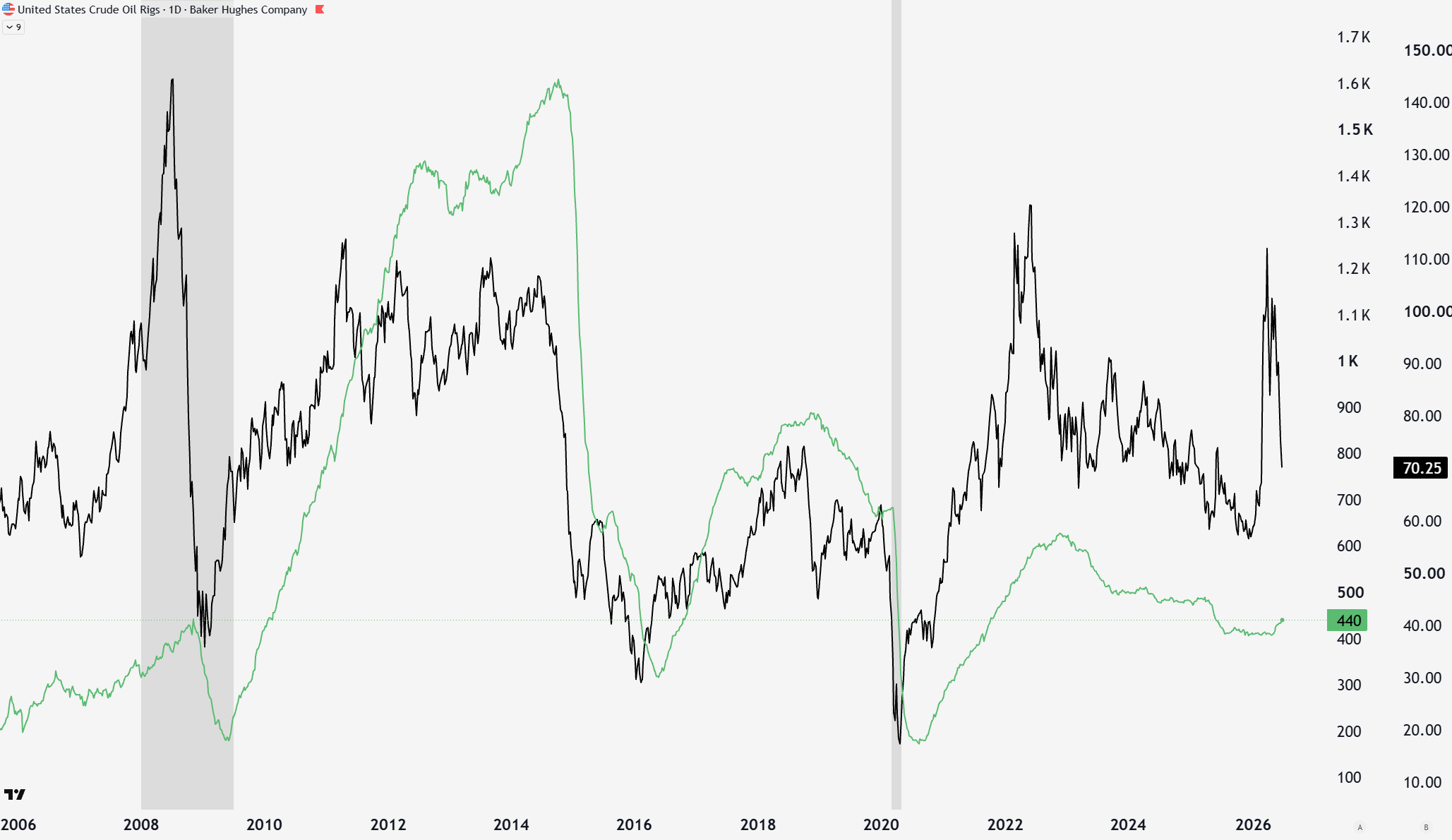

US producers still lack confidence to drill new wells after record-low oil prices during COVID. Rig counts show the willingness to invest in new drilling operations. They usually lag oil prices by 10-12 weeks. Following COVID, rig counts did not increase as aggressively as in the past, showing hesitation. Now, after the Iran conflict, oil prices went to $110/barrel, but rig counts have barely moved up. With prices back down near pre-war levels, this may lead to further hesitation.

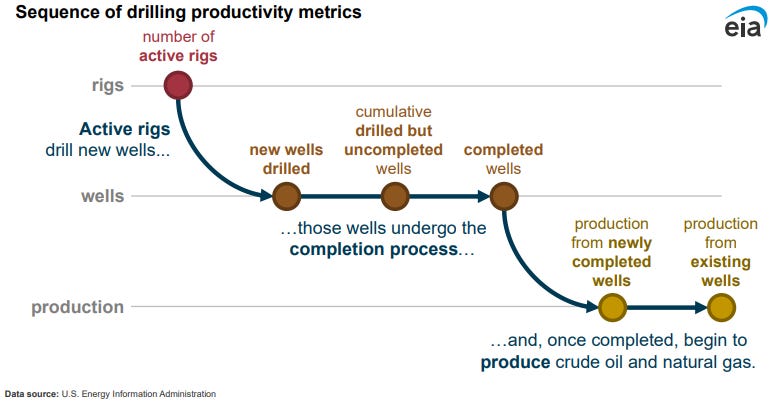

Rig count is merely the first step in the oil production journey. The rig needs to then drill the well and complete it before oil is produced.

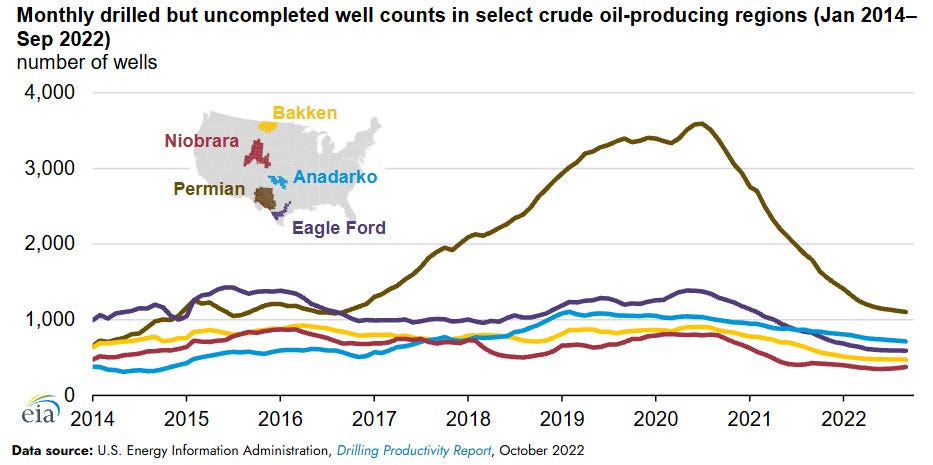

Considering rig counts lagged prices, the oil production growth in the past few years came from drilled but uncompleted wells. Instead of investing in new rigs and drilling new wells, they simply completed existing wells (DUCs). 78% of 2025 production came from wells that were already drilled. By late 2022, the buildup of DUCs was nearly exhausted. It is now harder for incremental oil production growth without significant investment, which we know companies are hesitant to do.

US production growth, while stalling, is also explained by efficiency gains. Fewer rigs and wells are producing more oil. While this sounds like a miracle, the truth is less rosy. As I discussed in No Love, companies are drilling further horizontally to get more out of each well. The headline is greater productivity per well, but the truth is lower productivity per lateral foot. On top of this, as the age of wells increases over time in the Permian, the share of gas extracted instead of oil increases, which is less valuable than the denser oil.

On the flip side, people point to potentially reduced oil demand as the reason for the drop. Oil demand tends to have greater impacts than supply unless supply is extreme. Demand for oil globally continues to increase and is revised higher each year. The other counterargument is that oil liquids have replaced some demand for crude oil. These liquids are not swappable one for one around the world, but switching certainly can happen at refineries if need be. Other than oil being manipulated or investor optimism, this is the real fundamental argument for lower oil prices.

All this to say the fundamental position of US production has not improved and is less responsive than it was. On top of that, reserves have been drawn down, and the foreign oil disruption has longer-lasting ramifications than people seem to realize.

Techincals

It’s hard to believe today, but oil used to be the top sector in the stock market not that long ago. Exxon was the largest US company from 2005 to 2011. It also held the crown from 1988 to 1994. An interesting cycle emerges, with alternating periods of energy vs tech dominance.

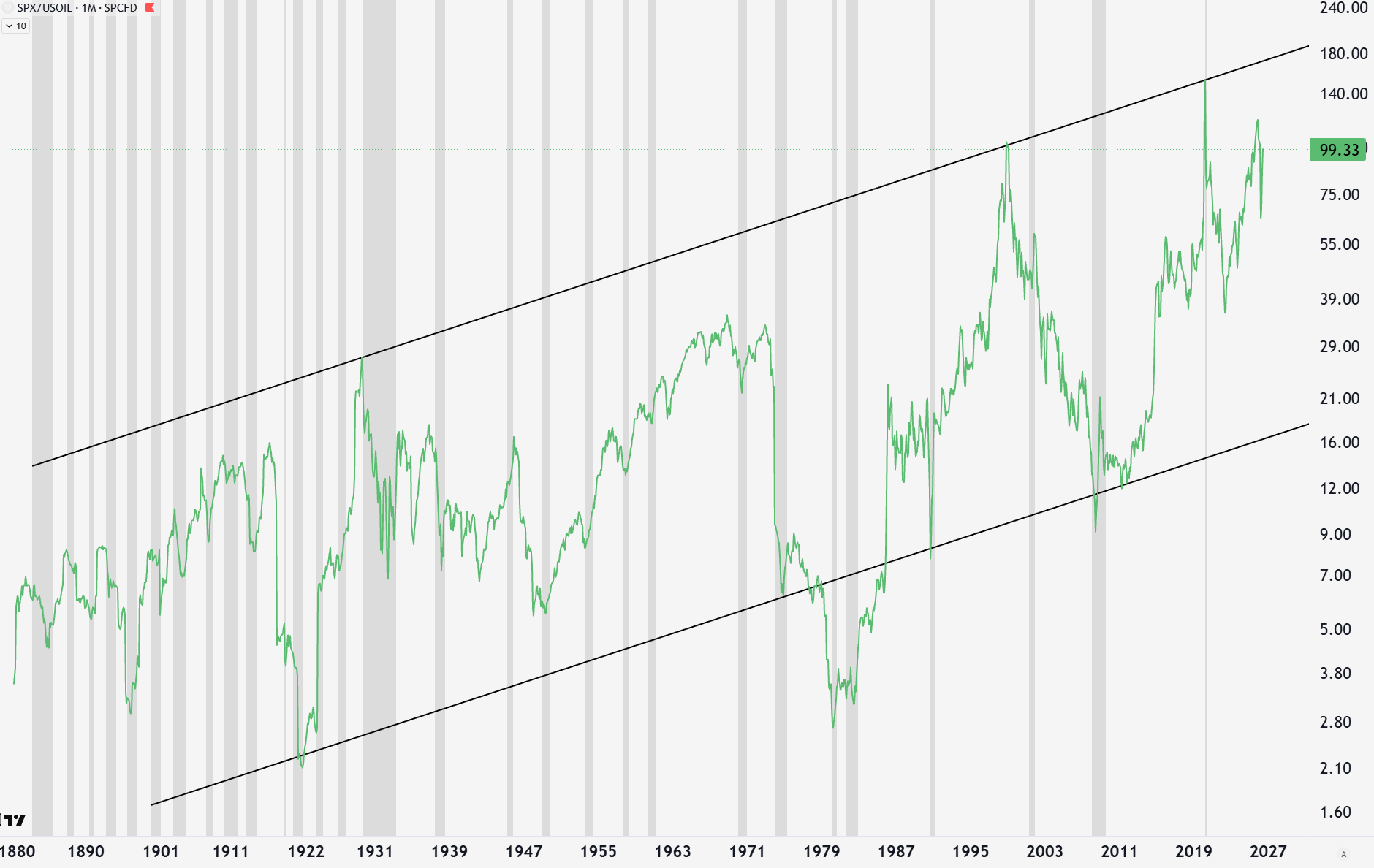

In 2011, energy was 11% of the S&P 500, and today it is a mere 3%. NVIDIA alone is over 7%, meaning one company is valued greater than the entire sector that fuels it all. The AI bubble will inevitably fall victim to its own malinvestment. The question is whether this value is vaporized or flows to other areas of the market. Historically, this has been the energy sector, which coincidentally is one of the most unloved sectors today. Priced in oil, the S&P 500 is very expensive.

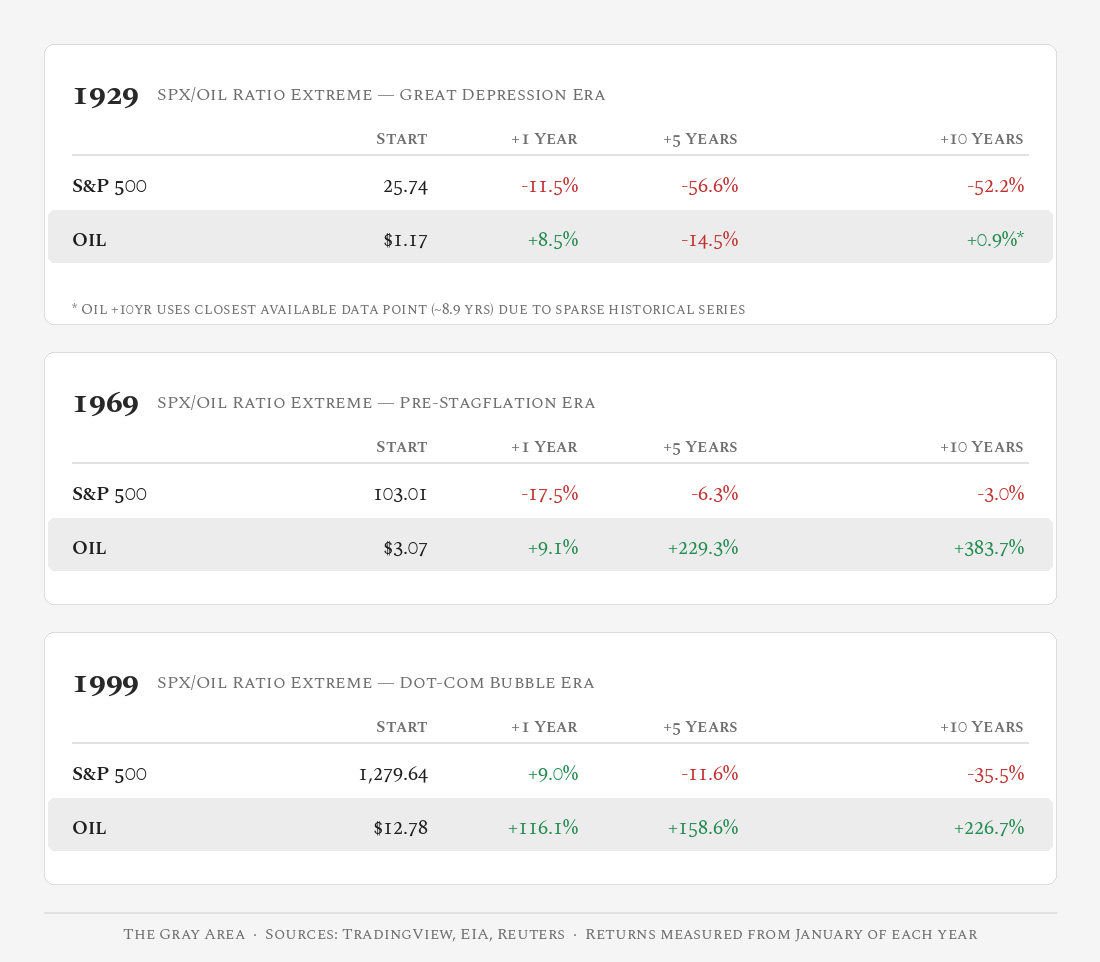

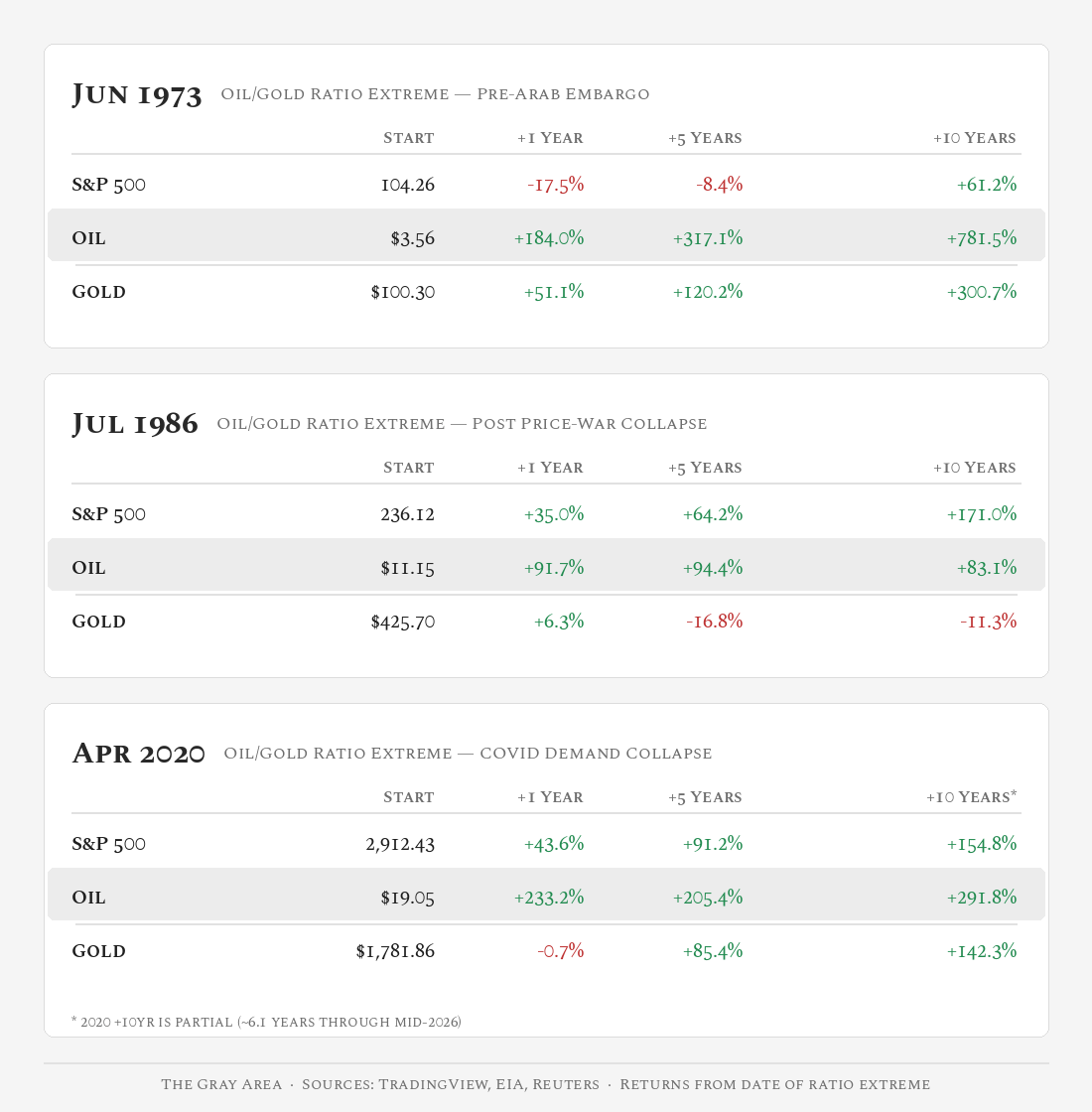

Levels near the upper trendline have only been observed a few times (1929, 1968, 1999, 2020, 2026). Comparing returns from these levels, you are way better off owning oil than stocks over a 1, 5, and 10-year period. Once again, we find ourselves talking about the three lost decades for stocks. While so far the 2020 extreme is bucking the trend, we might not have seen the peak just yet.

Pricing stocks in oil might seem funky, but we can also present oil’s relationship to gold. Among the commodity space, oil is historically cheap relative to gold. When the gold/oil ratio hits the upper trendline, this has also historically been a favorable time to invest in oil instead of gold. 2026 was another strike of this trendline. 1, 5, and 10-year returns for oil are historically favorable from these levels and most often outperform both stocks and gold.

The stocks in the energy space benefit from higher energy prices and increased flows into the energy sector. Already, tech companies (XLK) are spending capex like industrial companies but are priced as mega growth companies. At the same time, energy companies (XLE) are printing cash, may print more cash in the future in an oil bull market, and are not priced like it. The free cash flow yield for XLE is ~12%, while only ~4% for technology.

Conclusion

Oil companies are terrified to make investments in new oil production. You can’t blame them, given the downward price volatility from COVID and the Iran war peace deal. These and geopolitical actions have left the US in a more dangerous spot to truly respond to production in any meaningful way.

Based on nearly every metric, the stock market is in a bubble, led by the AI and technology sector. The energy sector has been extremely unloved. Typically, the energy and tech sectors rotate dominance, and we are at an extreme level now. It may take time, but I expect things to shift the other way. Buy oil and sell tech is the least sexy article in June 2026, but it is one that people may need to hear.

To learn how to participate in the market returns, truly diversify from various macro outcomes, and not get destroyed if the AI bubble pops, subscribe and get access to the Model Portfolio, which synthesizes all of these themes together.

-Grayson

Like to see these asymmetric opportunities synthesized into a real model portfolio that beats the S&P 500 and avoids major downside risks?

Socials

Twitter/X - @graysonhoteling

Email - thegrayarea55@gmail.com

Archive - The Gray Area

Notes - The Gray Area

Promotions

Sign up for TradingView

For educational and entertainment purposes only. The Gray Area should not be taken as financial advice.