Fields of Neglect

A confluence of factors could spell reversal in this unloved sector.

If you find this article interesting, click the like button for me! I would greatly appreciate it :)

The stock market is grossly overvalued according to metrics like the CAPE ratio and Buffett Indicator. Even defensive sectors and small value stocks trade at elevated valuations. With the outperformance of precious metals as of late, it seems like there aren’t many places left to put your money. Over the last few months, I’ve been looking for sectors that are neglected or have potential, like Oil and Uranium.

If an investment is exciting and popular, it likely means it is overbought technically and expensive fundamentally. The AI theme fits this bill perfectly, and even precious metals as of late. While momentum can carry those higher (and lower for the neglected ones) eventually, mean reversion will take place.

Today is about agricultural commodities. No one cares about wheat or sugar cane, especially since they’ve crashed roughly 50% in the last few years. There are three reasons to care, though: macro, climate, and technicals.

Macro

Crops today are not grown sustainably, but require copious amounts of industrial fertilizers due to the heavy tax the soil takes. In Phrosperous Land, I dive deeper into these fertilizers. In short, there are a few main elements that plants need to grow: phosphorus, nitrogen, sulfur, and potassium. The dominant phosphorus supply comes from Moroccan phosphate rock deposits, which are then primarily refined in China. Potassium comes from potash deposits, primarily in Canada, Russia, and Belarus. Sulfur compounds are mostly produced in China, North America, Russia, and the Middle East.

The last piece of the puzzle is nitrogen, consisting of urea, ammonia, and nitrates. Ammonia is the backbone of all nitrogen fertilizers, produced via the Haber-Bosch process with natural gas as key input. Anhydrous ammonia is a liquid, so transportation is difficult. Only in localized supply chains can farmers apply it directly. This is mostly a US phenomenon. Treating ammonia with carbon dioxide yields urea, an easier export, which goes to India, Brazil, Southeast Asia, and Africa. Finally, anhydrous ammonia can be treated and turned into nitrate compounds for easier transportation and application. These are primarily used in Europe and the United States. The US actually consumes about a third of each type.

The Middle East is one of the three main ammonia producers(other than Russia and China). Not only does the conflict in Iran affect the safe production of 33% of the world’s fertilizers (sulfur and nitrogen mainly), but the ability to export is also governed by the safe passage through the Strait of Hormuz. Further, disruption to oil and gas infrastructure in the region could disrupt natural gas, the dominant input cost to ammonium production. We stand at a critical time for the spring planting season. Without adequate fertilizers, crop yields will fall significantly. The regions most exposed to import issues are Brazil and India, followed by Southeast Asia, North Africa, and Australia. The US and Europe are protected but still affected.

This story could be nothing if the Middle East conflicts are short-lived like last time. It is never good to be too convinced one way or another when it is political decisions on the line. However, we have seen the deglobalization trends in other key resources like Uranium, base metals, and battery metals. Even if the immediate supply shocks subside for this planting cycle, the ever-divided global economy has the potential to price fertilizers higher. Furthermore, dull prices have caused farmers to project less planting in 2026. Lower crop yields on top of supply disrpution could be a recipe for higher prices if it plays out.

Climate

You’ve heard me talk about climatological impacts on agriculture before. In Not So Bright Pt 2, I discussed how solar cycles impact global weather patterns like the El Niño-Southern Oscillation (ENSO). ENSO events can be reliably predicted using the 11-year solar cycle and significantly affect the weather in South America and Southeast Asia. The effects extend globally, though, also affecting the US, Africa, and Europe.

Currently, European models indicate a +2°C anomaly, indicating a strong to very strong El Niño event. This is expected in the years following a solar maximum, but was not expected heading into this year. The anomaly is accelerating, and the predicted strength has been steadily increasing over the past few months, so it may not yet be fully appreciated.

If we reach +2 by summer as the model suggests, the ENSO anomaly would be one of the strongest in recent history, similar to the 1997/1998 and 2015/2016 El Niños. These periods drove significant food scarcity globally. Southeast Asia/Indonesia, India, and Southern Africa have the highest chance of negative outcomes. Sugar, wheat, rice, palm oil, coffee, and cotton may be affected. Certain crops, like sugar, may be affected in Brazil. El Niño moisture is typically helpful for most crops (i.e., soybeans) in the region, though.

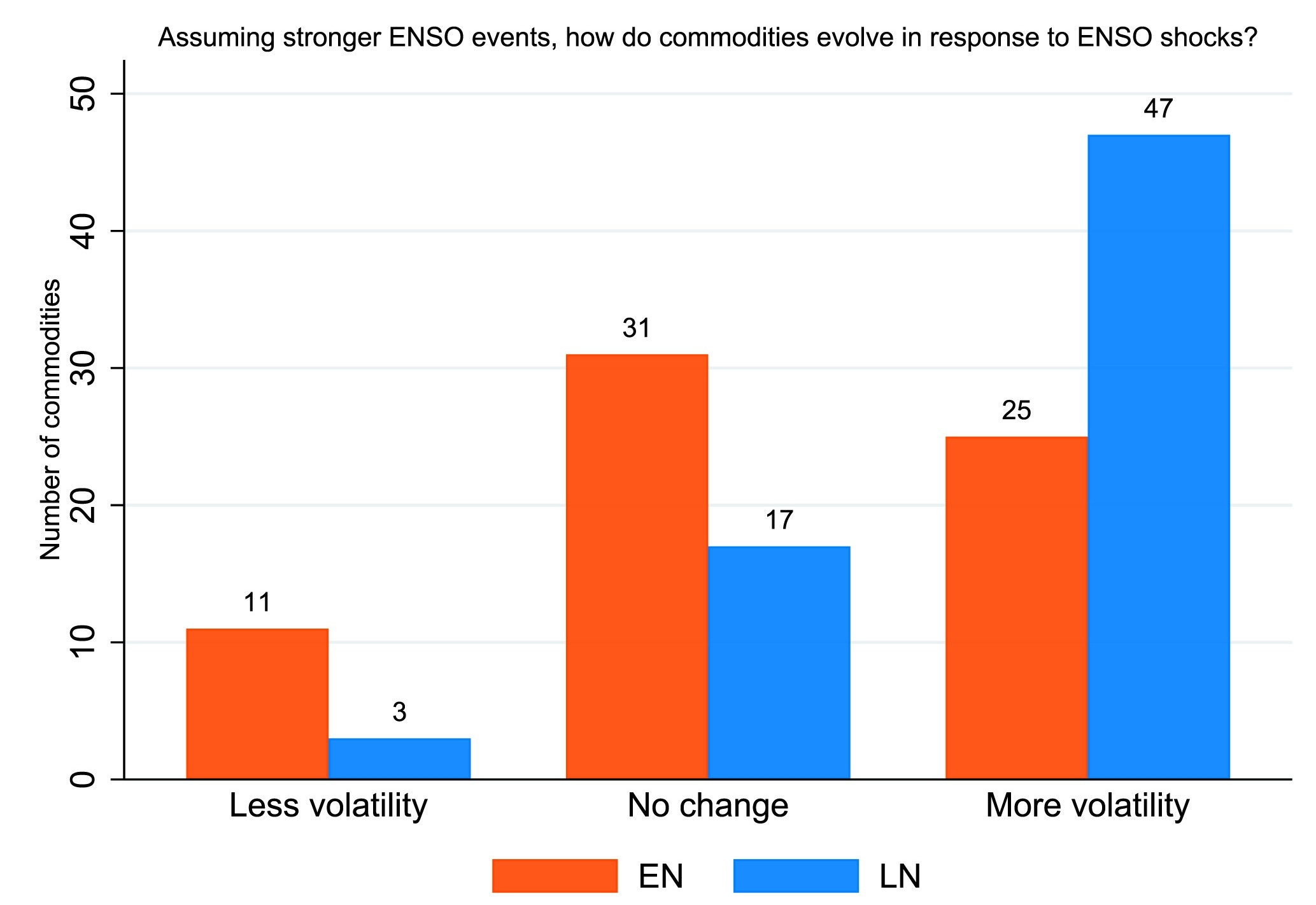

Dufrénot et al studied the climatological impact of stronger ENSO events on commodity price volatility. While they come from the lens of climate change affecting ENSO models, we can also view the statistically significant solar cycle impact as one that directly influences ENSO timing (not strength, except on larger cycles).

Their study suggests that there is a weak correlation between commodity volatility and ENSO during weak cycles; however, during strong ENSO anomalies, there is a significant increase in volatility. This doesn’t tell us price direction, just that prices will likely move more than normal.

Technicals

There are many different agricultural commodities, including sugar, wheat, corn, soybeans, cotton, cocoa, cattle, and palm oil. These differ from fuel commodities (oil, natural gas, coal), base metals (copper, zinc, aluminum), precious metals (gold, silver, palladium, platinum), rare earths, and battery metals. Gold, metals, and recently oil have experienced aggressive moves higher. Conversely, agricultural commodities have largely been oversold and sit below or near their 3yr moving averages.

Sugar, wheat, corn, and soybeans are considered the “cash crops”. Sugar is 2 deviations oversold relative to the 3yr mean, while corn, soybeans, and wheat are trying to breakout past the 3yr mean. Cattle is the opposite, 2 deviations oversold at all-time highs like most metal commodities. Cocoa just crashed from its exponential move higher in 2023. Palm oil has been rangebound for a few years and sits just above its 3yr average.

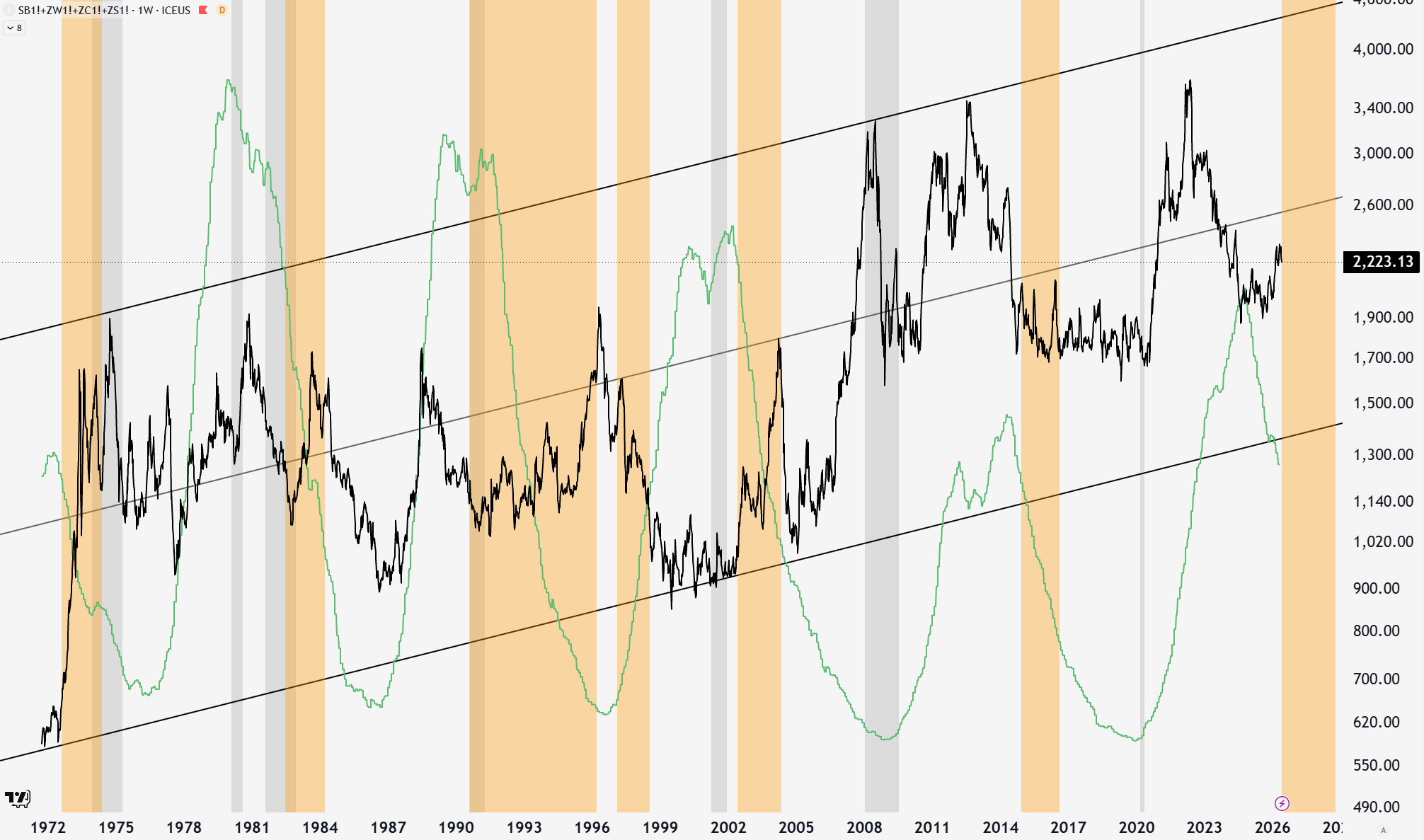

Relative to other assets in the market and to historic levels, agricultural commodities fit the definition of neglected and cheap. This is hard to come by these days. Below is a chart of the cash crops (sugar, wheat, corn, and soybeans). The chart is busy, but let me explain. The black lines form a price channel that has had range-bound prices since 1970. The green lines represent the solar cycle. The yellow shaded regions represent El Niño anomalies that followed the solar maximum.

Both times prices were at the lower bound, both soon revisited the upper resistance of the channel, appreciating 2-3x in price. Further, times when El Niño started with prices below the median line were also promising.

Even the price spikes in the 1862 Civil War time and 1917 WW1 time were off the back of a solar maximum and a strong ENSO anomaly. While these commodity spikes may have been catalyzed by the wars, there were agricultural consequences as well as the psychological impacts I discussed in Not So Bright.

Technically, agricultural commodities are near multi-year lows, under-owned, and already showing supply discipline from producers who can’t profitably farm at current prices. The setup for a mean-reversion from the lower trendline is there.

Fundamentally, the Middle East conflict has disrupted the global fertilizer supply chain at exactly the moment farmers needed inputs for spring planting. If not resolved soon, the full crop production impact of this fertilizer shock won’t be visible until harvest, if there are delays or crop yields are affected.

Climatologically, the solar cycle and current projects put a strong El Niño in front of us, a phenomenon that research associates with significant commodity price volatility. While it could take until next year to play out, together, there is a bullish case for agricultural commodities from here. Like any unloved sector, there could be more neglect, and recession could add further volatility depending on how things play out.

-Grayson

Socials

Twitter/X - @graysonhoteling

Archive - The Gray Area

Notes - The Gray Area

Promotions

Sign up for TradingView

You make a good case for buying ag commodities. Mike Swanson (WallStreetWindow.com) has been similarly encouraging this sector.