Written Off

Paper profits, deferred taxes, and the earnings bubble hiding inside the AI mania.

If you find this article interesting, click the like button for me! I would greatly appreciate it :)

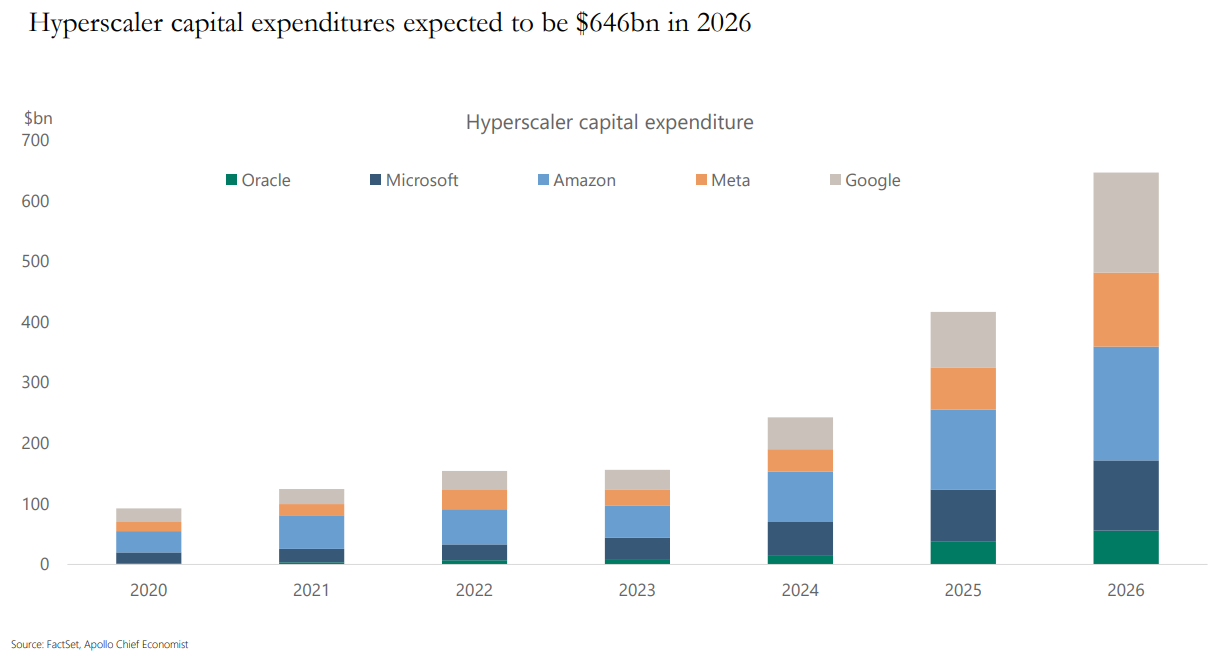

The stock market is in a bubble. From the Price/Earnings (P/E) ratio to the Buffett Indicator, valuations are at extremes. The stock market and economy are being driven by the AI boom. This boom is being driven by a narrow subset of the economy: hyperscaler capital expenditures (capex). This accounted for 96% of GDP growth in 2025; otherwise, growth would be 0.1% (a Harvard professor said it, not me). These high-margin, cash-flowing companies have decided to make considerable investments in building out data centers to supply AI models and cloud services. This number is already over $700 billion for 2026.

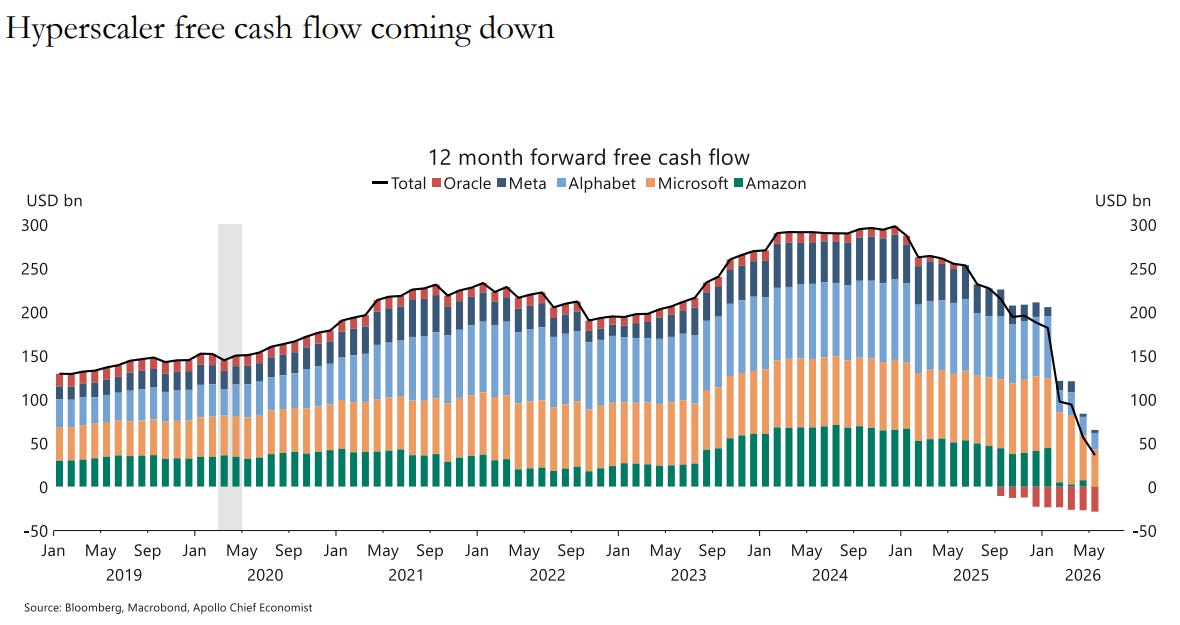

This capital expenditure comes from somewhere. Since these companies are successful and generate huge cash flows, they can funnel that directly into investments. Hyperscaler free cash flow was astronomic, but is now turning negative. If investments are productive and AI can be profitable, this will be worth it; otherwise, it could be a huge malinvestment. This is the million-dollar question investors are wrestling with.

For the past few years, companies have been issuing record share repurchases, or stock buybacks, instead of paying dividends or investing in new investments. Instead of boosting stock prices, companies actually investing in the economy and their businesses should be a good thing, right? Hopefully, and in theory, yes, it will drive future revenues. The AI narrative is a strong one, and this capex shows something real for investors to point to as a reason to pay higher valuations for these large US growth companies. However, it’s not the price (P) in the P/E ratio we should be concerned about; it’s the earnings (E).

Paper Profits

The stock market is historically a good investment because companies make earnings over time and grow. Earnings and earnings estimates for the hyperscaler companies are astronomical, with the rosiest expectations you could imagine from analysts. Unfortunately, there are a lot of accounting gimmicks going on.

If you invest in a factory, inputs, and labor and get out more in revenue, that's profit. Alphabet’s Q1 net income jumped 81% to $62.6 billion. 46% of that was merely marking up the value of its stake in Anthropic, one of the top AI companies. This is an unrealized, non-cash accounting gain sitting in the “other income” category. Amazon added a $16.8 billion gain in the same way. These paper profits accounted for a whopping 12% of the entire S&P 500’s earnings according to Mike Green.

This is perfectly legal and makes sense, but adds a layer of fragility if OpenAI and Anthropic’s valuations don’t continue to race higher forever. Google invests in an AI company, AI company valuation goes up, Google books additional earnings from AI company valuation. Google didn’t actually realize any earnings. When the Mag7 is 40% of the index, these things actually matter. As it accelerates earnings on the way up, it’s the opposite on the way down.

Capital F-light

One of the reasons tech companies are so richly valued is that they are capital-light and generate huge margins. An airline company is the example of the opposite; maintaining hangars, airplanes, maintenance equipment, and buying jet fuel is a lot of work. The hyperscaler companies had rapid scalability in software, ad platforms, etc with very little infrastructure. These companies are now investing large amounts into capex to provide compute and essentially become commodity companies. Build data center to sell compute = build oil rig to sell oil.

This capital requires capital… duh. Not only are they using cash flows to fund new investments, but they are also using debt. Oracle is the clearest example of this, projected to run out of cash by November if they don’t raise more capital. For the first time in years, following year after year of stock purchases, companies are selling stock as well. Google launched an $85 billion equity offering, one of the first mega-caps to sell stock in a while.

My long-time readers know I am privy to the passive investment phenomenon. Google, Meta, along with IPOs of SpaceX, Anthropic, and OpenAI, means there will be more supply for these money flows to soak up than there has been in a long time.

Circularity

One of the most touted AI bear arguments is the circular financing. Also common for Cisco during the dot-com boom, Nvidia invests in a company on the assumption it will then buy the chips from Nvidia. Nvidia has used stock to invest in Coreweave, just so they can buy GPUs from Nvidia. When Nvidia, OpenAI, and Oracle all pass $100 billion back and forth, it only works if OpenAI becomes profitable.

Mike Green estimates Nvidia’s earnings are overstated by about 300%. If true and earnings per share (EPS) is a quarter of reported EPS ($6.56 TTM becomes roughly $1.64), at $195 and a P/E of 30, it implies price should be $49, or -75%. When the bubble pops, people won’t be willing to pay as high a multiple either, so if the P/E drops to 15x, that leaves price at $25 or -87%. Crazy? Cisco was the Nvidia of the internet and fell 90%.

Everything is fine and dandy as long as someone is giving OpenAI and Anthropic money to buy things. As soon as Nvidia, the hyperscalers, and other private equity stop, they will have to use their own money, if they have some by then. In the meantime, this is boosting Nvidia earnings and making everything look better than fine, even encouraging more investment.

Depreciation

The One Big Beautiful Bill Act restored 100% bonus depreciation for qualifying property, like GPUs, servers, cooling, and electrical systems. This lets hyperscalers deduct the full cost of AI infrastructure in year one for tax purposes, rather than spreading it over five or six years. This tax deferral lets companies pay tax later instead of now, leaving more cash on the balance sheet the year the investments are made.

On top of this potentially spurring further investment and tax deferral, there are debates on how much GPUs actually depreciate given the technological advancement. Will GPUs in data centers be obsolete in 4-6 years or shorter? This not only has tax implications, but real implications for investment. Costs rise for companies having to constantly fund new capex to stay afloat. Here brings us to the airline company vs software company again. Are the hyperscalers going to have to keep maintaining and buying new infrastructure like Delta?

Regardless, the government has lowered the tax cost of data center investments where the useful life is contested, all while circular financing and private investments are boosting earnings.

Obsolescence

Investors are paying premiums on these companies like they know the forward returns will be there to match. We can also speculate on a future where things are not as they seem today. No one knew where the dot-com boom was headed even though we knew it would change the world. We shouldn’t be so naive today. If we’re so optimistic about these companies, why not be optimistic about the technology itself?

Just this year, Chinese models have reduced costs by over 90%. This has led many companies to move compute to these cheaper open source models. Further, if efficiency gains and hardware technology keep improving, we could do a lot with less. It is not infeasible to imagine a world where we don’t actually need data centers. On-device or decentralized architecture using a fraction of today’s compute could leave this a huge malinvestment in hindsight. What if the question isn’t how long the infrastructure will last, but if it is even the right infrastructure in the first place?

I may sound like a doomer, but I am actually more optimistic on AI than most investors. This is speculation, but I think we see energy and hardware efficient models that can be used for the majority of users on smaller devices as hardware and models improve. Like railroads and fiber, this leaves tremendous compute capacity being built out with a much smaller market than originally forecasted.

Conclusion

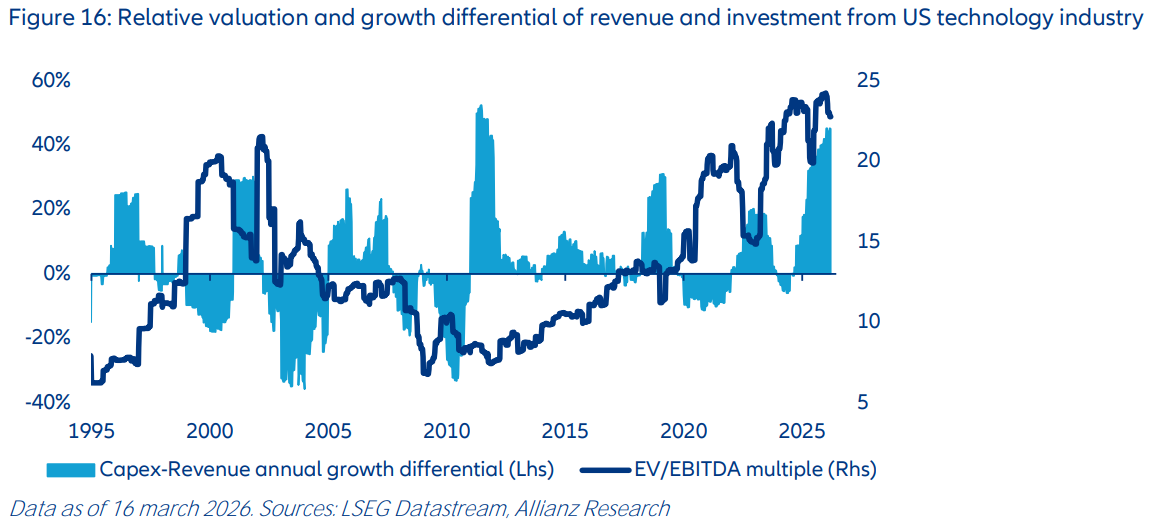

The hyperscalers are spending more money than they are making in revenue. Whether that investment turns into revenue is the million-dollar question. The capex-to-revenue growth rate is 46% and higher than the dot-com peak. At the same time, the enterprise valuation is higher than that period as well. These are extremes on every metric.

If it looks like a duck and quacks like a duck, it’s a duck. There is no doubt we are in an AI bubble, but the bubble is even bigger than people realize because the earnings are a bubble too. This causes the P/E ratio to look smaller and more attractive as you’re dividing by a bigger number.

Earnings ended up cut ~30% in the 2000 dot-com bust, and ~50% during the 2008 financial crisis. Assuming earnings were merely 10% lower in reality, the P/E ratio goes from 41 to 46, surpassing the dot-com peak of 44. If earnings were 30 or 50% lower in reality, the P/E would be 60 or 83. These three scenarios where earnings are lower imply 40%, 53%, and 86% drawdowns to return to the long-run average P/E of ~28.

AI will change the world like the internet, perhaps even more so, but that does not mean earnings and valuation bubbles don’t go through mean reversion. If OpenAI and Anthropic are both profitable, hooray, but Netscape and AOL paid the price for their success in time. Even Cisco, Sun Microsystems, and Yahoo all were crushed when the bubble popped. Cisco generated massive free cash flow each year through the dot-com period, but it didn’t stop its stock price from falling 90%. New paradigms don’t go predictable ways, as I said. The hype landscape (Netscape, AOL, Sun Microsystems, Yahoo) gave way to the real winners that ate the leftover scraps (Google, Microsoft, Verizon, eBay).

Eventually, people realize they don’t need as many railroad tracks, internet servers, and eventually AI compute. Nvidia will still be a cash flow monster, but bubbles always pop. It took 21 years for Cisco to recover its high, and I suspect a similar fate for Nvidia.

The AI bubble is built on misleading earnings, driven by hype around transformative private companies with questionable futures. These misleading earnings are priced for perfection, at the highest valuations only seen in the 1929 bubble and the 2000 dot-com bubble.

Expect the unexpected. AI will transform in ways the world is not looking at right now. Most importantly, don’t bet your wealth on a market that destroyed investors in 1929 and 2000. We are in that same market now. If you want to keep growing wealth and not be collateral damage, subscribe to see the model portfolio and learn how to make it through the AI bubble and 4th turning.

-Grayson

Like to see these asymmetric opportunities synthesized into a real model portfolio that beats the S&P 500 and avoids major downside risks?

Socials

Twitter/X - @graysonhoteling

Email - thegrayarea55@gmail.com

Archive - The Gray Area

Notes - The Gray Area

Promotions

Sign up for TradingView

For educational and entertainment purposes only. The Gray Area should not be taken as financial advice.